This week with the rise and growing interest in Digital Asset Treasury companies, we deep dive Strategy, formerly known as Microstrategy.

Let’s dive into Strategy MSTR 0.00%↑ with our fundamental analyst, Kevin Li.

Executive Summary:

Bitcoin is entering its institutional era, catalyzed by the 2024 approval of spot ETFs and growing global adoption. It remains early in its transition to a mainstream store of value.

Strategy’s core thesis is built on Bitcoin’s long-term CAGR, projected to decline gradually from ~40–50% today to inflation-aligned returns over time, with most gains driven by fiat debasement and increasing institutional allocation.

Strategy operates as a Bitcoin-backed securities company, not just a holding vehicle—using convertible bonds, preferred equity, and ATM share offerings to acquire more Bitcoin with non-callable, long-term capital.

Convertible bonds provide upside-aligned liquidity, enabling Bitcoin purchases today in exchange for future equity—structured to appeal to hedge funds through volatility arbitrage and delta-neutral strategies.

Preferred equity opens access to the $46T U.S. bond market, offering fixed-income instruments backed by Bitcoin, tailored for institutional investors seeking yield with inflation resistance.

The ATM equity program enables real-time capital raising, allowing Strategy to issue shares at a premium (mNAV > 1) to accretively increase Bitcoin per share when investor sentiment is high.

Strategy’s equity is now a financial product, offering customized Bitcoin exposure across the risk spectrum—from high-volatility equity to fixed income products—designed for diverse institutional mandates.

The flywheel works if Bitcoin’s CAGR > cost of capital. If this condition fails, dilution and leverage risks rise. Execution discipline, brand trust, and institutional confidence are essential for sustaining growth.

Part 1: The Bitcoin Thesis

Before we begin evaluating Strategy, it's essential to first establish the Bitcoin thesis. The foundation of Strategy’s strategy is built entirely on the long-term CAGR (Compound Annual Growth Rate) of Bitcoin over the next decade. Bitcoin is currently transitioning from a nascent, marginal asset class to a mainstream, core component of the global financial system—a shift that effectively began in 2024 with the approval of spot Bitcoin ETFs. As of now, we are in Year 2 of that transition and we are still early.

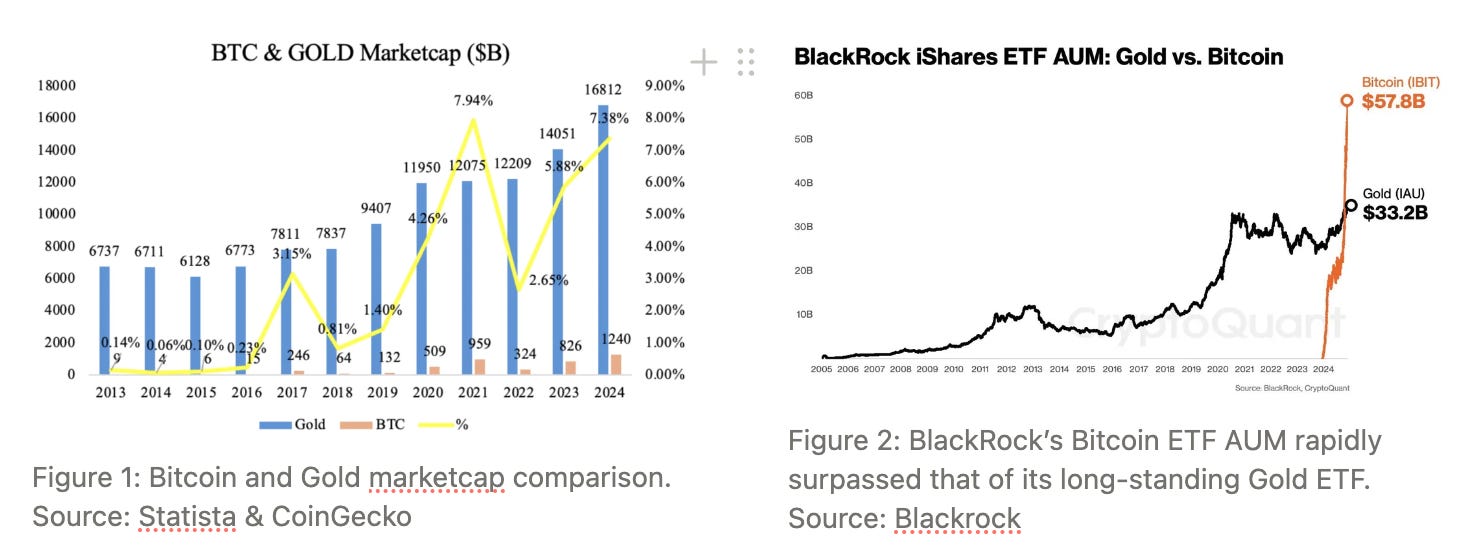

To put things in perspective: Bitcoin has already broken above $100K and surpassed its previous all-time high. Yet, it still sits at only around 7% of gold’s market capitalization—which gold itself is near record highs due to soaring demand driven by global uncertainty. This heightened interest in gold is not a headwind for Bitcoin, but a sign of growing appetite for store-of-value assets, a trend that directly benefits BTC as it continues to mature and gain institutional traction. Furthermore, BlackRock’s Bitcoin ETF AUM surpassed that of its decade-old gold ETF within its first year—highlighting the accelerating shift in investor preference toward Bitcoin as a modern store of value.

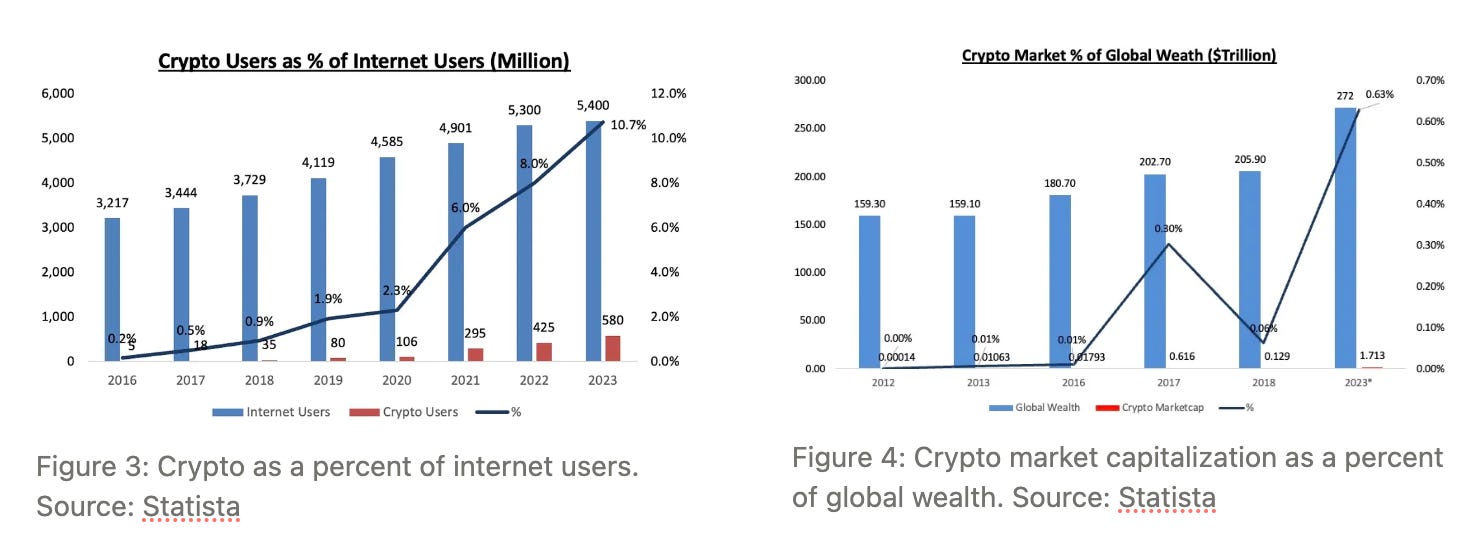

Furthermore, we’re seeing rapid adoption of crypto among users, with crypto users now making up nearly 10% of global internet users (as of 2023). However, crypto’s share of global wealth remains just 0.63% (as of 2023), highlighting the significant growth potential still ahead for the broader crypto asset class—and Bitcoin in particular.

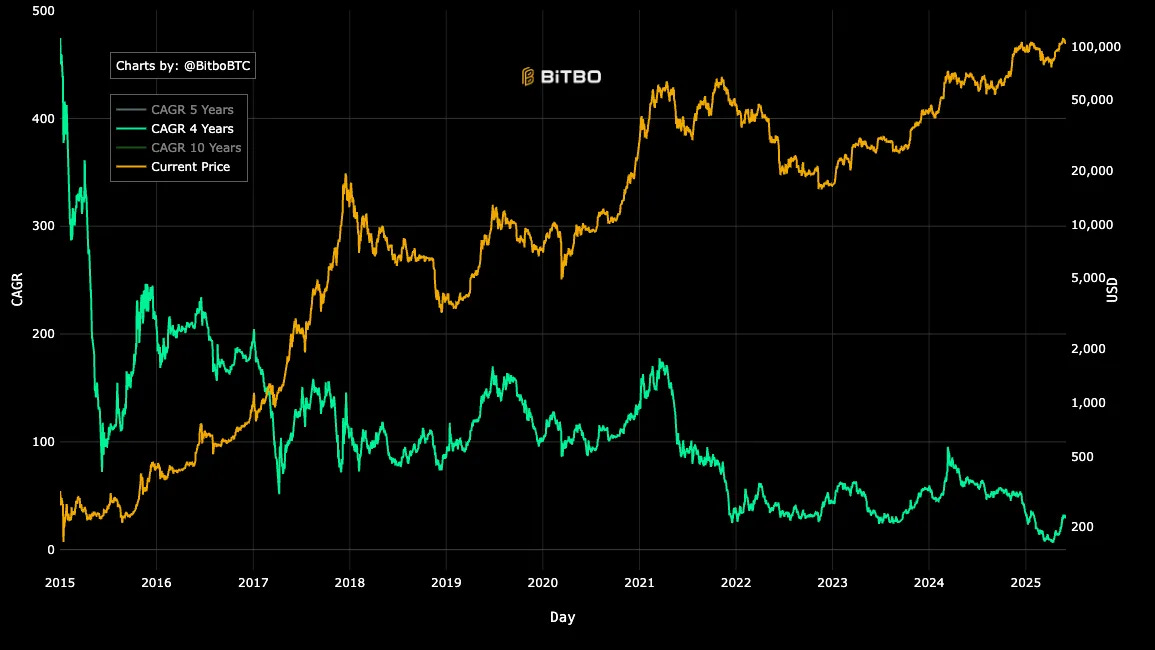

Historically, Bitcoin's CAGR exceeded 100% in its early years. However, as adoption grows and the asset matures, its CAGR has been gradually declining, now sitting in the 40–50% range. Over the next 10 years, we anticipate a continued decline in CAGR as Bitcoin becomes increasingly institutionalized—likely falling from 50% to 40%, then to 30%, 20%, and eventually converging with the inflation rate as it becomes a fully integrated financial asset.

Figure 5: Bitcoin 4 year CAGR change over time. Source: BiTBO

Part 2: Understanding the price driver of Bitcoin

Bitcoin, as a scarce and non-productive asset, is influenced by two primary long-term factors:

Depreciation of Fiat Currencies(Inflation): The continuous expansion of fiat money supply, particularly the U.S. dollar, has led investors to seek assets that can serve as a hedge against inflation and currency debasement. Bitcoin, with its fixed supply of 21 million coins, is increasingly viewed as a viable store of value in this context. In Michael Saylor’s interview with Lex Fridman, he articulates this thesis clearly: the real inflation rate of the U.S. dollar over the past 100 years has been closer to 7–8% per year, not the 2% commonly reported by government sources. According to Saylor, the government systematically adjusts the Consumer Price Index (CPI)—through changes to the basket of goods and hedonic adjustments—to understate true inflation. Meanwhile, real inflation “shows up” in asset prices such as housing, stocks, and bonds—areas excluded from CPI.

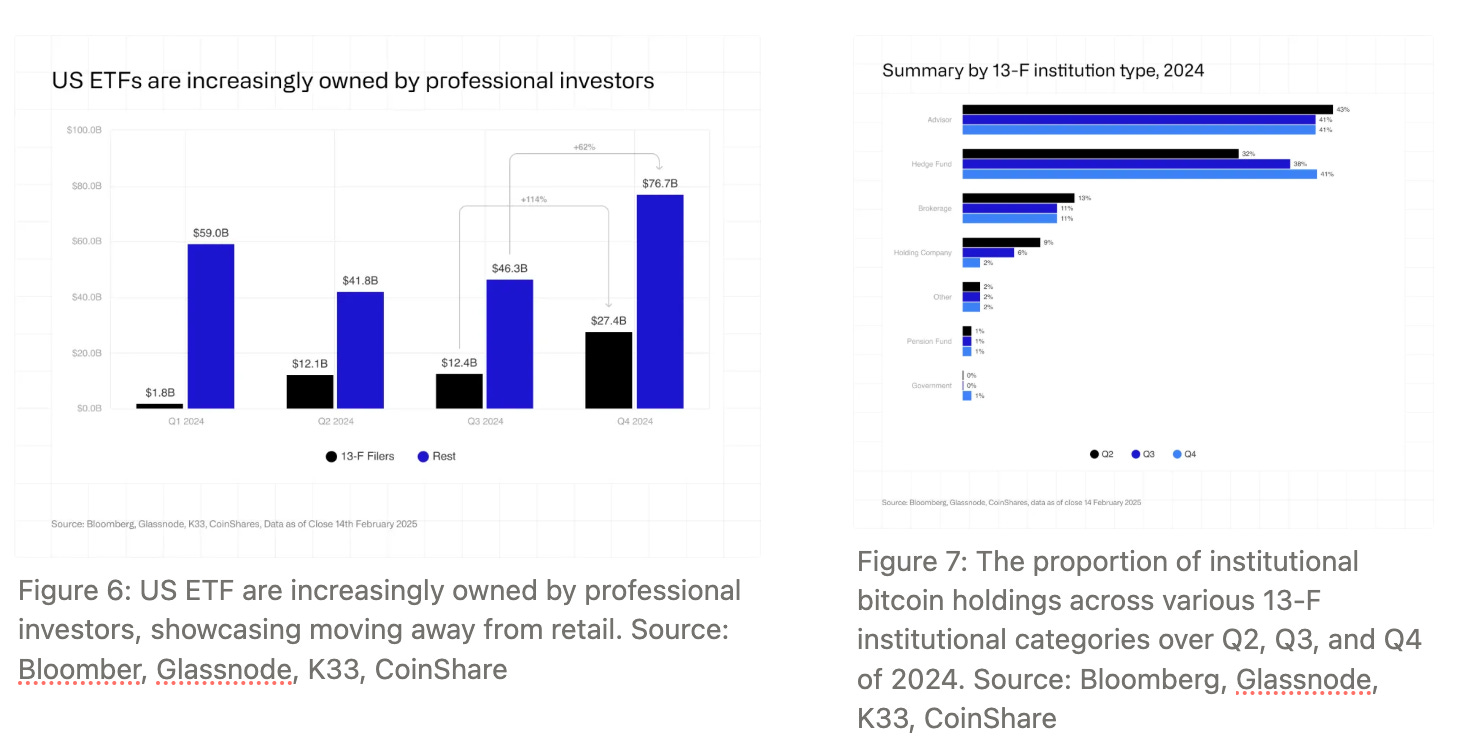

Global Investor Preference for Bitcoin as an asset class: Another key price driver for Bitcoin is the percentage allocation of investors’ portfolios to Bitcoin as an asset. Importantly, ETFs serves as a bridge between the crypto ecosystem and global financial markets, offering a secure, regulated, and scalable vehicle for capital to flow into digital assets. According to CoinShares and Bloomberg, U.S. Bitcoin ETFs are increasingly held by professional investors, with financial advisors and hedge funds leading the charge. While pension fund involvement remains limited for now, their potential entry could represent the next major wave of adoption.

With this understanding established, if Bitcoin’s CAGR averages 40% annually, it is estimated that approximately 7–8% of that growth can be attributed to fiat currency depreciation, while the remaining 32–33% is driven by increasing investor allocation to Bitcoin as an asset class. This breakdown is critical to understanding the long-term investment thesis of Strategy and will be revisited later in our analysis.

Introduction to Strategy: A Toolkit for Accessing More Capital

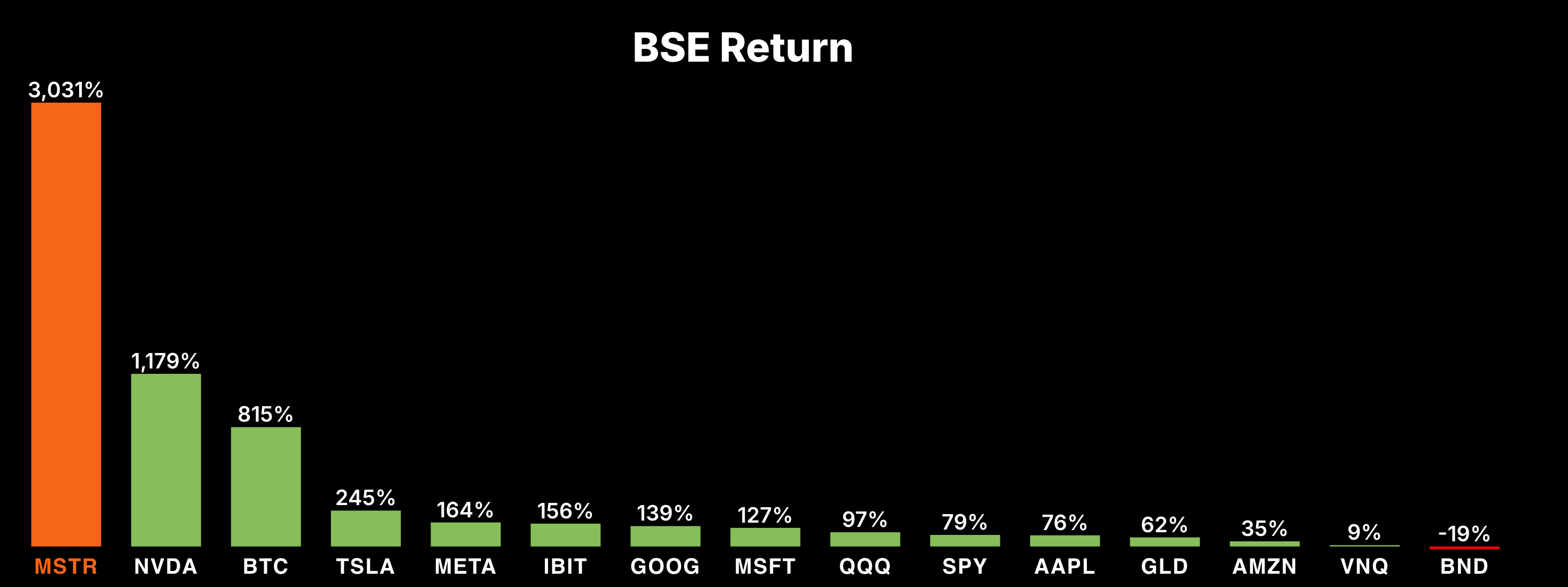

Originally a business intelligence and analytics platform, Strategy is now best known for its pioneering role in corporate Bitcoin adoption. Since 2020, the company has aggressively accumulated Bitcoin as its primary treasury reserve asset. As a result, its stock has outperformed all members of the 'Magnificent Seven' and has become one of the top-performing stocks since adopting this strategy.

Figure 8: Showcasing MSTR outperformance over BTC Source: Strategy

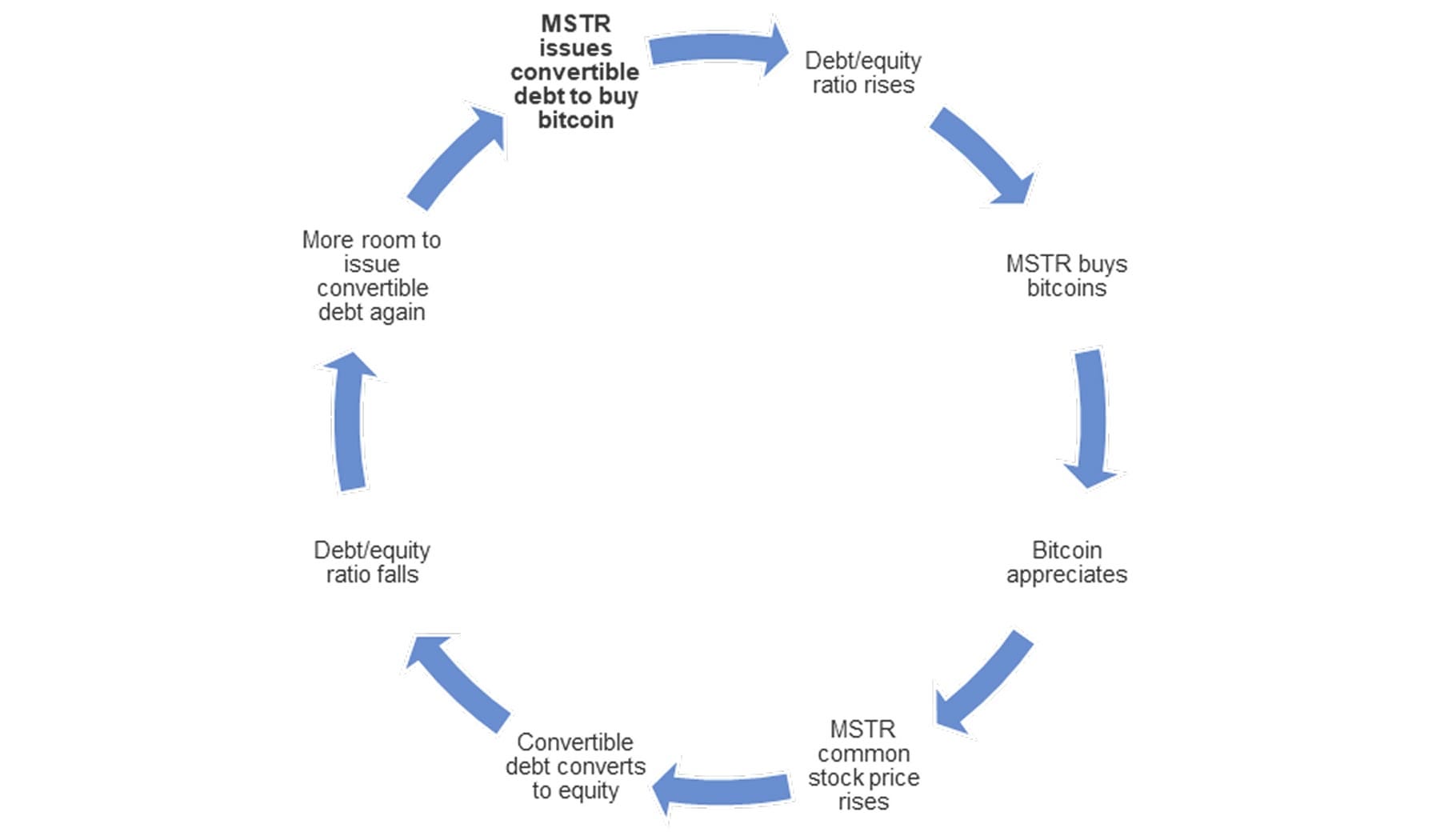

While Strategy may appear to be merely a Bitcoin holding company, a closer look reveals it functions more like a Bitcoin-backed securities company. At its core, Strategy seeks to tap into various forms of NON-CALLABLE liquidity in the financial markets to acquire more Bitcoin. In doing so, it has effectively launched a new sector—what could be called the 'Bitcoin Treasury Corporation'—with the singular goal of increasing Bitcoin per share of a publicly traded stock. Currently, there are 3 main methods that Strategy uses to gain more liquidity to buy more Bitcoin:

Convertible Bonds – Raises capital by issuing debt that lenders can convert into stock, using the proceeds to buy more Bitcoin.

Preferred Equity – Raise capital by issuing preferred equity that pays fixed dividends to investors annually.

At-the-Market Offering (ATM) – Sells new shares directly on the open market to raise flexible, real-time funding for buying Bitcoin.

Strategy’s Convertible Bonds

The first tool that Strategy used to access liquidity was convertible bonds(CBs). These are debt instruments that allowed the company to borrow non-callable funds, typically on a four-year term, with minimal annual interest. Each bond includes a conversion price—a target stock price at which the debt can be converted into equity. If Strategy’s stock does not reach that price, the company must repay the principal along with interest at maturity.

This structure is particularly appealing to institutions seeking long exposure to Bitcoin with reduced risk. Furthermore, some institutions, restricted by mandate from directly purchasing Bitcoin, can still gain indirect exposure by investing in these CBs. As Bitcoin’s price rises, Strategy’s stock typically appreciates as well, allowing bondholders to convert their bonds into equity and capture the upside. In a downside scenario, investors still receive principal and interest, offering a more balanced risk-reward profile. Historically, these CBs have even outperformed Bitcoin’s spot performance.

Since CBs function essentially like long-term call options, if they are converted, Strategy is effectively selling its stock at a higher future priceand using that liquidity to buy Bitcoin today—this is where the value accrual occurs for Strategy. What’s even more interesting is that, due to the structure of these bonds, Strategy’s stock becomes safer as its stock price appreciates. This is because the company gains the ability to convert outstanding debt into equity, effectively eliminating those liabilities from its balance sheet. Additionally, if the stock price exceeds 130% of the conversion price for a set period, Strategy can force bondholders to either redeem for shares or accept repayment in cash.

It’s important to emphasize that these bonds are unsecured, meaning they are not backed by collateral. Even if Bitcoin were to drop by 90%, Strategy is not at risk of a margin call—as long as the price recovers by the bond’s maturity date. To manage this risk, Strategy has strategically spread out the maturity dates of its bond issuances, typically spreading them across two Bitcoin cycles, making the repayment risk more manageable over time.

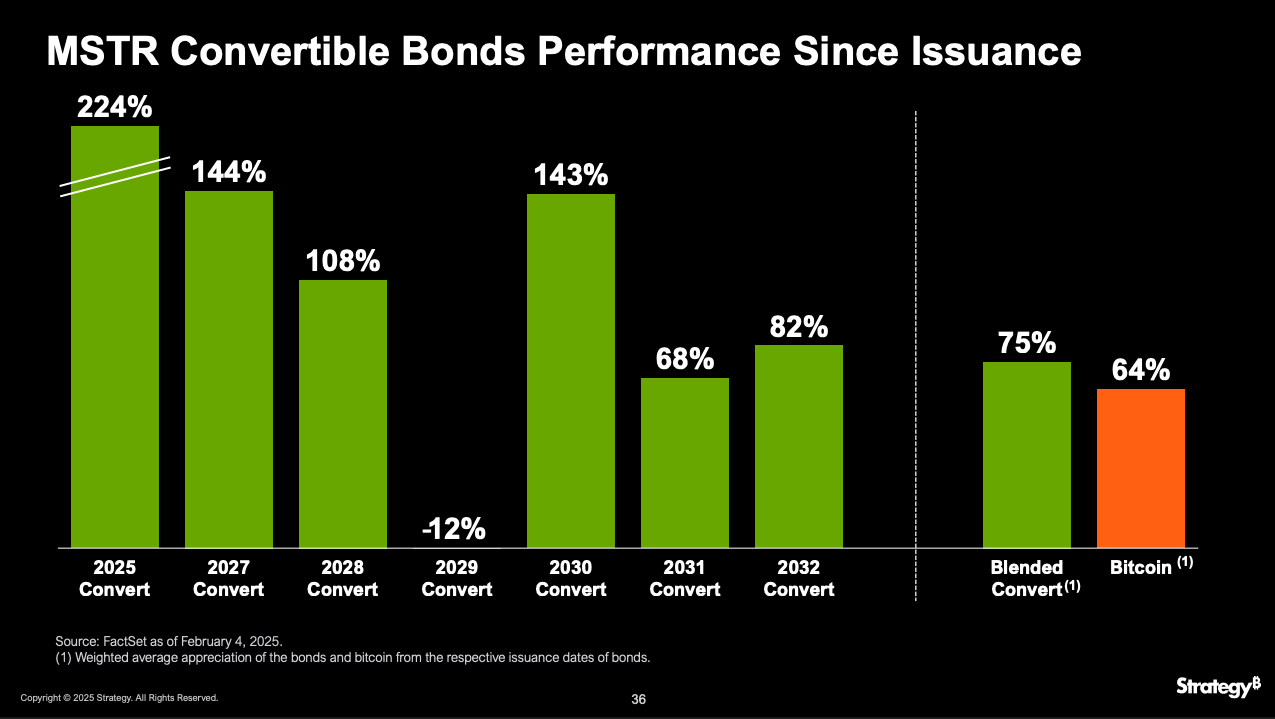

Figure 11: Current Strategy convertible bonds issuance, highlights convertible bonds issued with low interest (coupon) rates, and maturity dates spread across multiple Bitcoin market cycles. Source: Strategy

As Strategy ventures into new financial territory, it has effectively found a way to package its stock’s volatility as a product and sell it to institutions through convertible bonds—often in exchange for zero-coupon terms (as shown above). When Strategy issues convertible bonds to purchase Bitcoin, it’s essentially leveraging debt to acquire a volatile asset. This leverage increases the volatility of its own stock, as the company takes on margin-like risk.

Since convertible bonds (CBs) are priced like options, institutional investors (hedge funds in this case) typically hedge their exposure by shorting Strategy’s stock when buying the bonds. This creates a delta-neutral position, eliminating directional risk while maintaining exposure to both realized and implied volatility. Hedge funds then profit through gamma trading and gains from vega exposure, capitalizing on Strategy sharp price swings and leveraged balance sheet.

Hedge Fund Arbitrage Walk Through Example: For example, if the stock rises from $400 to $500, the bond’s delta may increase from 0.7 to 0.9. To stay delta-neutral, the fund shorts more shares at $500. If the stock later drops back to $400, they cover the new short, locking in a profit. However, if the price keeps rising, the bond's value offsets losses on the short. These swings—can occur multiple times per month—can generate consistent profits. As Strategy issues more debt, its stock becomes more volatile, which can increase the CBs’ value through higher implied volatility. This creates a compelling arbitrage opportunity for hedge funds.

Ultimately, the convertible bonds (CBs) create a win-win situation for both Strategy and the CB buyers: hedge funds can arbitrage the volatility, while Strategy gains access to future liquidity today.

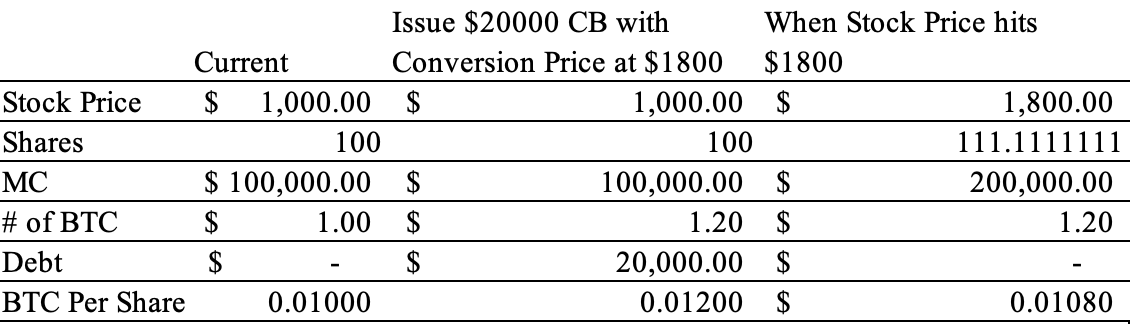

Here is the unit economics for Strategy’s CB value accrual as an example:

Figure 12: An example to show the increase in Bitcoin per share through the conversion of convertible bonds.

In this example, we assume Strategy stock price is $1,000 with 100 shares outstanding, and the entire $100,000 market cap is invested in Bitcoin at a price of $100,000 per Bitcoin—meaning the company holds 1 Bitcoin. Next, Strategy issues a $20,000 convertible bond (CB) with a conversion price of $1,800. It uses the proceeds to buy more Bitcoin, increasing its total Bitcoin holdings. When the stock price reaches $1,800, the bond converts into equity, increasing the share count from 100 to approximately 111.11 shares ($20,000 / $1,800). After conversion, the company’s Bitcoin holdings have increased, and Bitcoin per share rises from 0.01 to approximately 0.0108—indicating value accrual for shareholders.

Strategy’s Preferred Equity

The next step for Strategy to access greater liquidity was its preferred equity offering—structured as fixed-income-like products aimed at the much larger fixed income market. For context, the U.S. convertible bond market is valued at around $270–280 billion, while the U.S. fixed income market totals roughly $46 trillion—about 100 times larger in available liquidity.

Strategy currently offers three types of Preferred Equity:

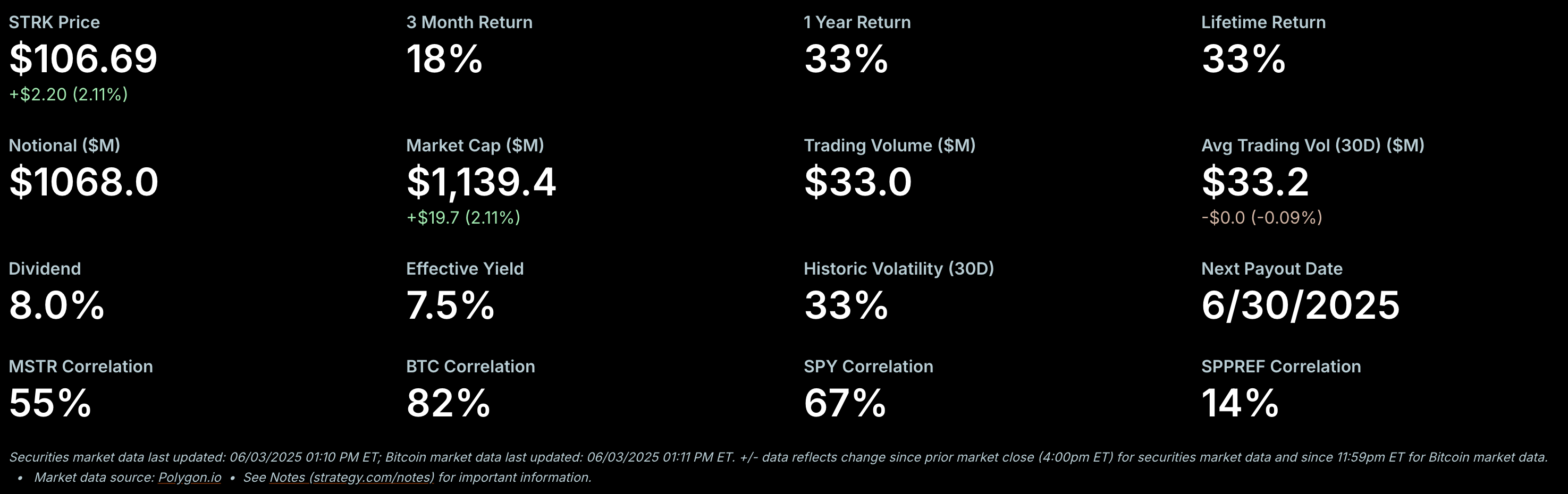

STRK – Series A Perpetual Strike Preferred Stock – Offers 8% yield, convertible, callable shares, providing long-term funding for Bitcoin accumulation.

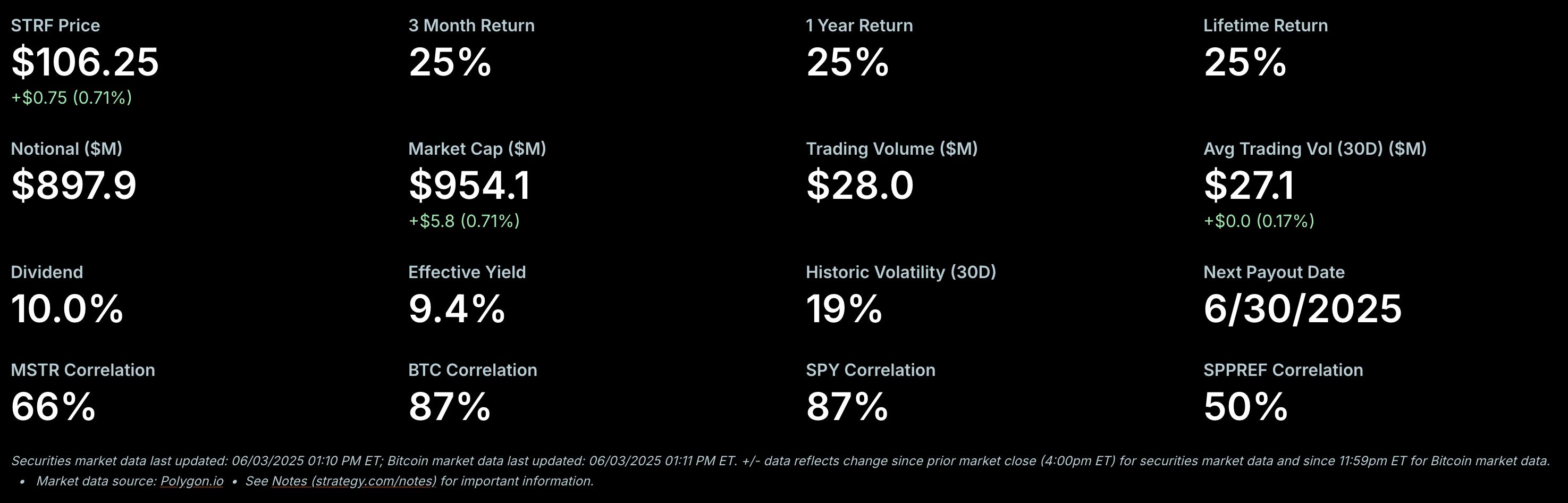

STRF – Series A Perpetual Strife Preferred Stock – Offers 10% yield, non-convertible, non-callable shares, ensuring stable, long-term capital for Bitcoin purchases.

STRD – Series A Perpetual Stride Preferred Stock – Offers 10% yield, non-convertible, callable shares, providing stable, long-term capital for Bitcoin purchases.

Each is priced at a $100 par value. STRK pays $2 quarterly ($8 annually), while STRF and STRD pay $2.50 quarterly ($10 annually). STRK is also convertible, with a $1,000 MSTR stock conversion target, offering holders potential upside exposure to both MSTR and Bitcoin. In contrast, STRF is non-convertible and non-callable—providing a higher, steady return but with no upside participation. The key difference between STRF and STRD lies in callability and dividend treatment: while STRD also offers a 10% yield, it is callable and pays non-cumulative dividends—missed or delayed payments do not accrue, increasing investor risk. STRF, on the other hand, pays cumulative dividends—any missed payments accrue with interest and must eventually be paid by Strategy.

Figure 13: Strategy’s CBs and preferred equity on balance sheet, representing only 9% of company’s market capitalization, indicating controlled leverage. Source: Strategy

The pricing of STRK is influenced by both the risk-free rate and the market price of MSTR. As MSTR approaches $1,000, the value of STRK should increase due to its convertible nature. Additionally, in finance, return is relative. If the risk-free Fed Funds rate falls from the current range of 4.5%–5% to a lower range of 2%–2.5%, the theoretical return on STRK should decrease to around 4%. For this to happen, the market value of STRK would need to rise to approximately $200 per share to reflect the reduced yield and maintain price equilibrium.

This creates two clear upside scenarios for STRK holders:

Falling interest rates – As rates decline, STRK appreciates in value.

Rising MSTR price – If MSTR hits $1,000, STRK benefits due to its conversion feature.

As Jeff Parks puts it, STRK is “the perfect financial product.” Investors receive an 8% annual return while positioned to benefit from either a rate decline or MSTR appreciation. Even without either catalyst, the investor still earns back their principal through the 8% annual yield over time.

Figure 14: STRK’s performance and trading statistics showcases a high-performing fixed income product. Source: Strategy

By contrast, STRF and STRD are priced solely based on the risk-free rate. Should the risk-free rate fall to 2%–2.5%, these securities would similarly be expected to trade closer to $200 to reflect a new yield of approximately 5%, down from the current 10%.

Figure 15: Similarly, STRF’s peformance and trading statistics also showcases a high-performing fixed income product. Source: Strategy

However, STRD is typically priced below STRF, resulting in a higher yield. This is because STRD is callable first and its dividends do not accrue, meaning investors are not guaranteed the stated dividend if a payment is missed. This structural difference justifies the yield premium investors demand for holding STRD over STRF. However, since the dividends comes from MSTR stock issuance, as the prices of both MSTR and Bitcoin continue to rise, the relative impact of annual interest payments on total share issuance becomes increasingly negligible—resulting in minimal dilution over time.

Here is the unit economics for a STRK preferred equity as an example:

Figure 16: An example to show the increase in Bitcoin per share through the issuance of STRK

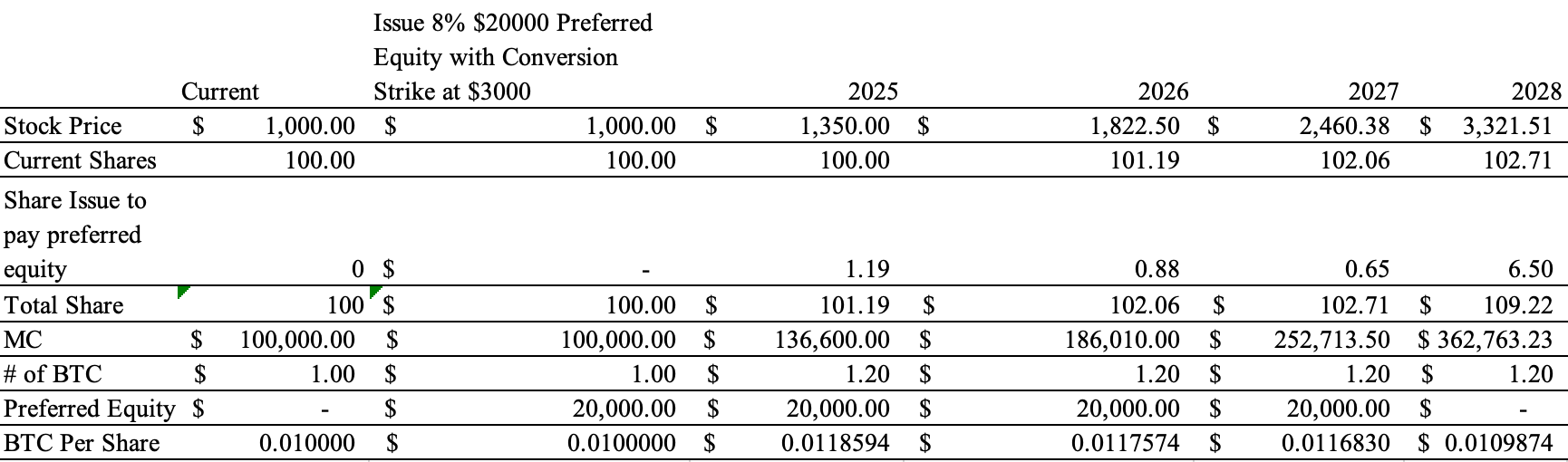

In this case, MSTR’s stock price begins at $1,000 and grows at 35% annually, starting with 100 outstanding shares and a $100,000 market capitalization—all backed by a single Bitcoin. The company raises $20,000 by issuing 8% preferred equity, which is used to acquire additional Bitcoin.

Each year, the 8% interest on the preferred equity is paid to STRK holders by issuing new MSTR shares. The preferred equity carries a conversion price of $3,000. By 2028, the stock price reaches $3,321.51, triggering full conversion of the $20,000 preferred equity into common equity.

As new shares are issued each year to pay interest and upon conversion, the total share count increases. The Bitcoin per share is recalculated annually based on updated total Bitcoin holdings and share count. By 2028, the Bitcoin per share has increased from 0.01 BTC/share to 0.0109874 BTC/share—representing nearly a 10% increase. This highlights how the strategy of using preferred equity to accumulate more Bitcoin can enhance the per-share Bitcoin exposure, even after accounting for dilution.

As previously mentioned, fundamentally, the price of Bitcoin is driven by two core factors: monetary inflation and growing preference for Bitcoin as an asset. Strategy’s approach with these preferred equity products essentially forgoes some of the inflation-driven upside in exchange for providing a yield to preferred shareholders—specifically inflation-linked returns in the case of STRK. This structure allows the company to arbitrage the dividend paid on the preferred equity against Bitcoin’s annual compounded growth rate (CAGR). As long as Bitcoin's CAGR exceeds the effective cost of capital (e.g., 8–10%), these preferred equity instruments are economically beneficial. In this sense, the newly structured preferred equity offerings are like truly inflation-proof bonds, making them attractive instruments for fixed income portfolio managers seeking hard asset-backed yield exposure.

Here is the unit economics for a STRF preferred equity as an example:

Figure 17: An example to show the increase in Bitcoin per share through the issuance of STRF. It’s important to note that shares issued to pay dividend decreases exponentially.

The unit economics of STRF and STRD closely mirror those of STRK, with one key distinction: STRK fully converts to equity by 2028, while STRF is perpetual and STRD is callable at the company’s discretion.

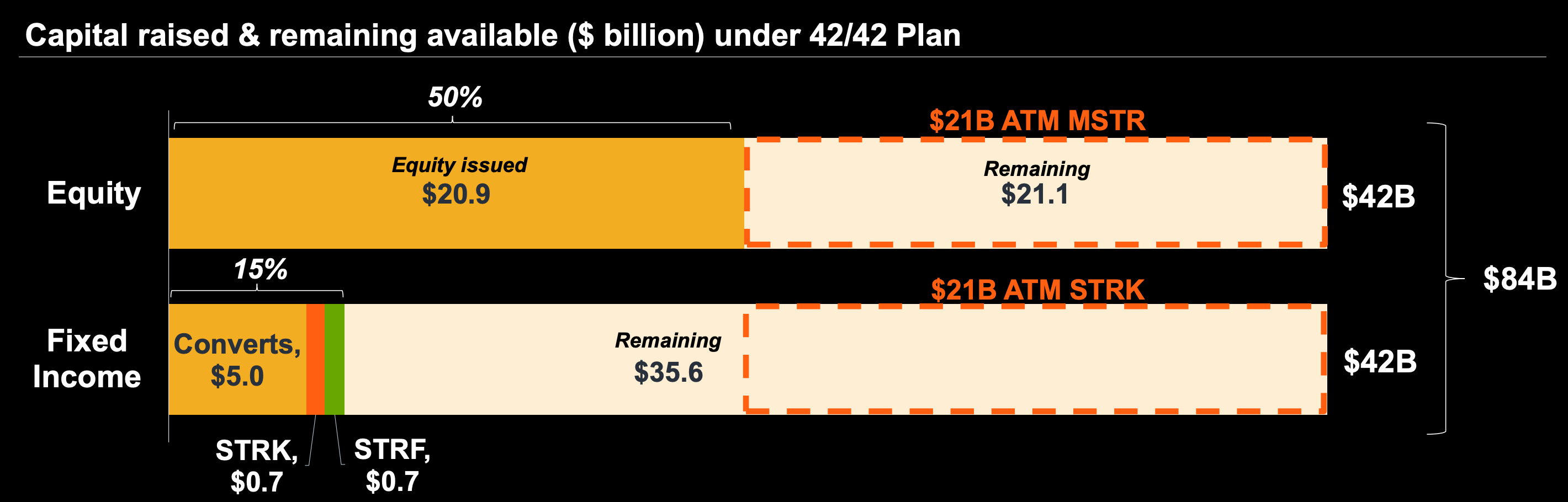

As of 2025, Strategy appears to favor preferred equity as its preferred method of taking on leverage. One key advantage is that preferred equity typically has no maturity date, avoiding the pressure of refinancing or repayment risk. Additionally, the annual interest rate on this preferred equity is relatively minimal when compared to the company’s market capitalization and the scale of its operations. Implicitly, this strategy suggests that Strategy is positioning itself for a long-term Bitcoin supercycle, rather than a traditional four-year Bitcoin cycle.

Figure 18: In Strategy’s new 42/42 capital plan, Saylor has focused on fixed income product, particularly STRK. Source: Strategy

Strategy’s At-the Market Offering

The third but arguably most important/used tool in Strategy’s liquidity kit is its At-The-Market (ATM) equity program. Unlike convertible bonds or preferred equity—which are structured, negotiated securities—the ATM program allows Strategy to sell newly issued shares directly into the open market in real time, typically through a designated broker. This provides the company with flexible, on-demand access to capital based on current market conditions.

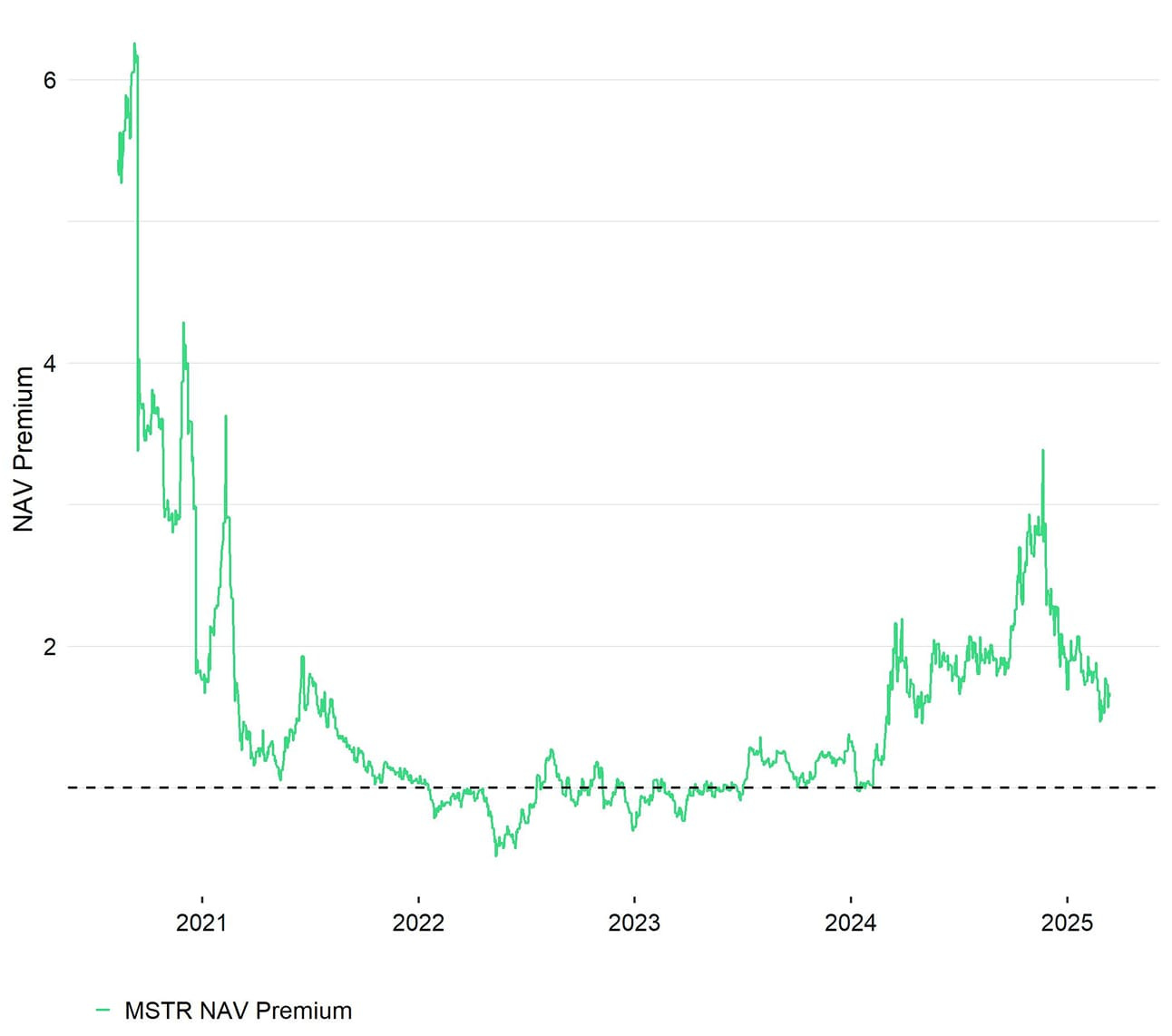

Due to its use of convertible bonds and preferred equity, Strategy has successfully earned a premium over its net asset value (NAV), as investors believe each share will represent more Bitcoin in the future. Furthermore, this NAV premium is influenced by Strategy’s leveraged balance sheet and the volatility it generates. This premium is dynamic—it may expand or contract depending on broader market liquidity and investor risk appetite. When risk-on sentiment dominates and Strategy’s strategy is in favor, the premium widens. When markets tighten or sentiment fades, it can compress. Strategy can capitalize this volatility through its ATM program.

Figure 19: Strategy Stock NAV premium change over time. Source: Bitwise

When the mNAV (multiple to NAV) is greater than 1—due to this volatility and market optimism—issuing new shares becomes value-accretive. Strategy is effectively selling shares that represent less Bitcoin than what the company can acquire with the proceeds, increasing Bitcoin per share. In this way, the ATM program is not just a funding tool—it’s the execution trigger for Strategy’s capital flywheel, enabling the company to respond in real time to favorable market conditions and expand its Bitcoin position with high capital efficiency.

Part 3: Equity as a Product & Growth Engine

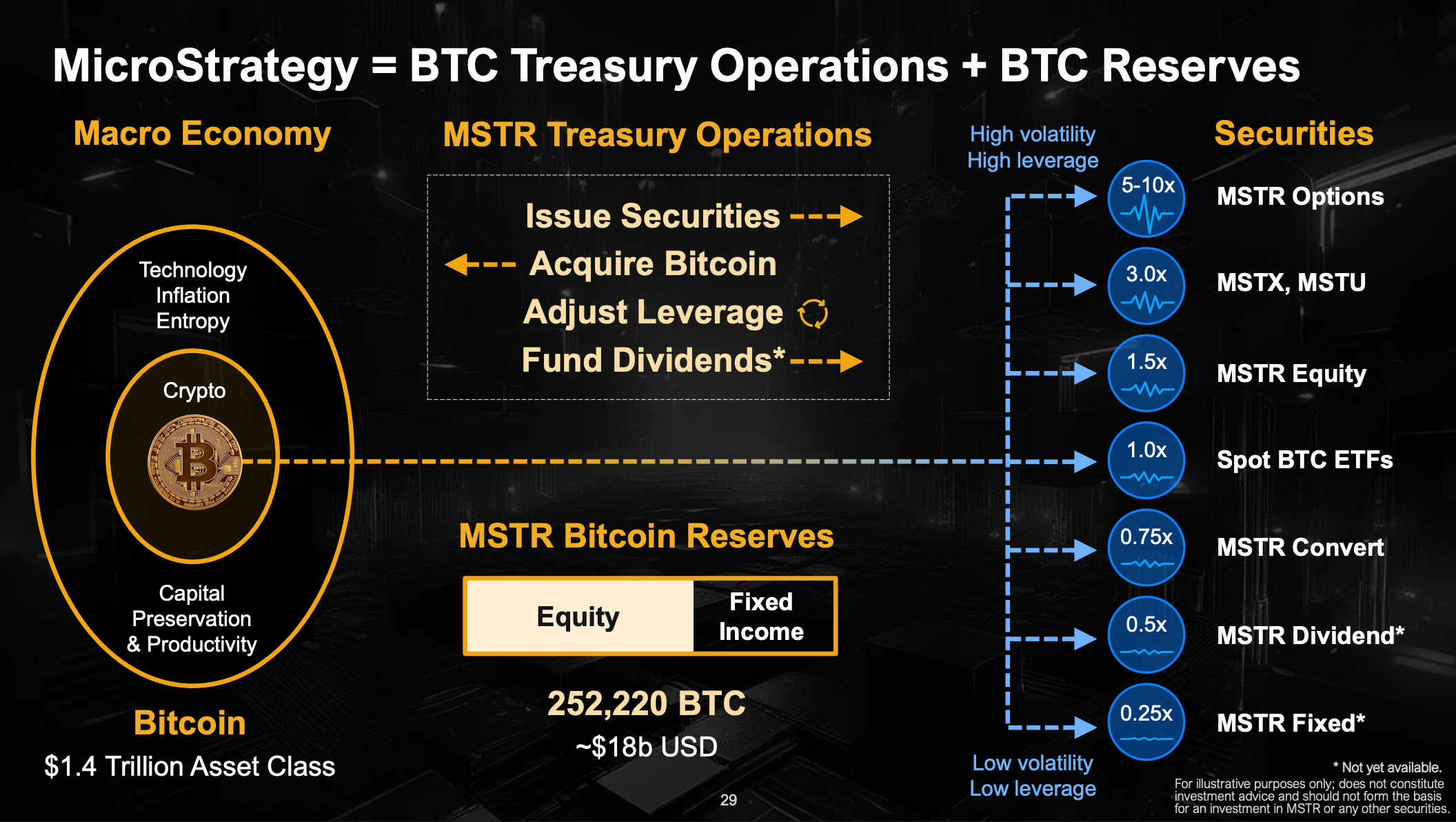

This ability to issue equity above NAV—in effect, selling volatility today in exchange for Bitcoin—reveals a deeper insight: Strategy’s equity is no longer just equity. It has become a financial product. For its debt products, the value doesn’t accrue at issuance—it accrues when Strategy sells shares at a future-aligned price and uses that liquidity to buy Bitcoin now. In essence, the company is offering a new kind of security: future/premium MSTR shares backed by Bitcoin, structured to capture forward-looking BTC exposure with institutional leverage.

Productized Bitcoin Through Equity Wrappers for Different Investor Types

As briefly discussed in the convertible bonds section, Strategy’s real innovation lies in its ability to productize Bitcoin exposure into customized, compliant financial products—using its secondary equity as a structural wrapper. Pension funds, insurance companies, endowments, and bond portfolio managers are often prohibited by mandate from holding Bitcoin directly. By issuing convertible bonds and preferred equity, Strategy unlocks access for these institutional investor profiles to gain indirect exposure to Bitcoin.

Figure 20: New securities that is formed by MSTR equity backed by Bitcoin. Source: Strategy 2024 Q3 Investor Presentation

Moreover, the return and volatility needs of these institutions vary widely. A bond portfolio manager isn’t going to allocate to a crypto asset with a 40% annualized return if the volatility is also 40%. They would much rather hold a preferred equity instrument offering a 10% IRR with only 10% volatility. That’s why Strategy’s capital instruments—CBs and its different preferred equity classes—are intentionally structured to offer different risk/return profiles.

At one end of the spectrum, MSTR equity offers the highest expected return and volatility. At the other, STRF offers the lowest return and lowest volatility, functioning more like a fixed-income instrument. In between, CBs and other preferred products provide exposure tailored to specific institutional risk appetites, effectively making Strategy a menu of Bitcoin-wrapped securities for every risk profile.

Volatility is Vitality

Volatility is a critical component of Strategy’s flywheel. On one hand, MSTR can capitalize on elevated volatility by issuing equity through its ATM program when the mNAV is high, effectively monetizing its premium. On the other hand, higher volatility improves the pricing of convertible bonds, as it increases the value of the embedded call option.

Additionally, increased volatility boosts the liquidity of MSTR stock, its options, and derivative products, enabling hedge funds to engage in gamma trading strategies and structure zero-coupon convertible bonds. The greater the volatility, the more profit potential from gamma trading, further reinforcing institutional demand. Finally, leveraged products such as MSTZ and MSTX benefit from this liquidity dynamic. They allow for more exposure and, in doing so, draw additional capital into the Strategy equity ecosystem, enhancing overall market depth.

mNav is the Engine Fuel

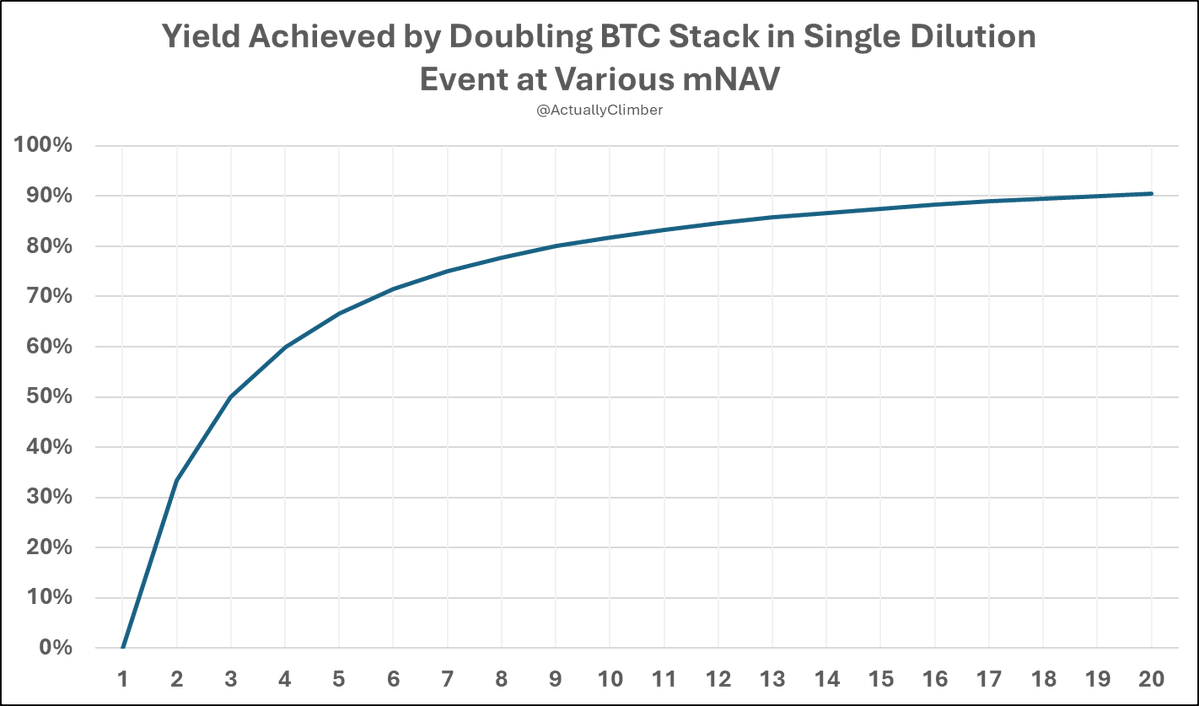

The mNAV is the fuel that ignites Strategy’s Bitcoin accumulation. In our unit economics models for CBs and fixed-income products, we assumed an mNAV of 1. But when the company issues equity at a premium—mNAV > 1—it compounds value even faster, enabling it to raise more capital on better terms and increase BTC per share more efficiently.

Figure 21: A higher market NAV (mNAV) results in slower dilution when acquiring Bitcoin and leads to a greater increase in Bitcoin per share. Source: X @ActuallyClimber

Why the Market Pays the Premium

Several factors contribute. First is the expectation that the company can acquire more BTC per share via liquidity raised through CBs and preferred equity. Furthermore, early in this strategy, regulatory constraints prevented many institutional investors from holding BTC/BTC ETF directly, making Strategy a proxy. This proxy value remains relevant depending on the institution profile. Second, brand trust is critical: do institutions trust the company’s financial products? Does retail buy into its narrative? Both play a role in sustaining the premium, as equity becomes the engine of the strategy. Strategy excels in communicating its vision to both institutional and retail investors. There's also a strong first-mover advantage — being the first to offer a secure, trusted BTC-backed equity product builds brand equity that competitors struggle to match. Institutions are unlikely to back convertible bonds or preferred equity issued by second-tier players — credibility and market leadership matter deeply in this space.

Passive Inflows: The ETF Feedback Loop

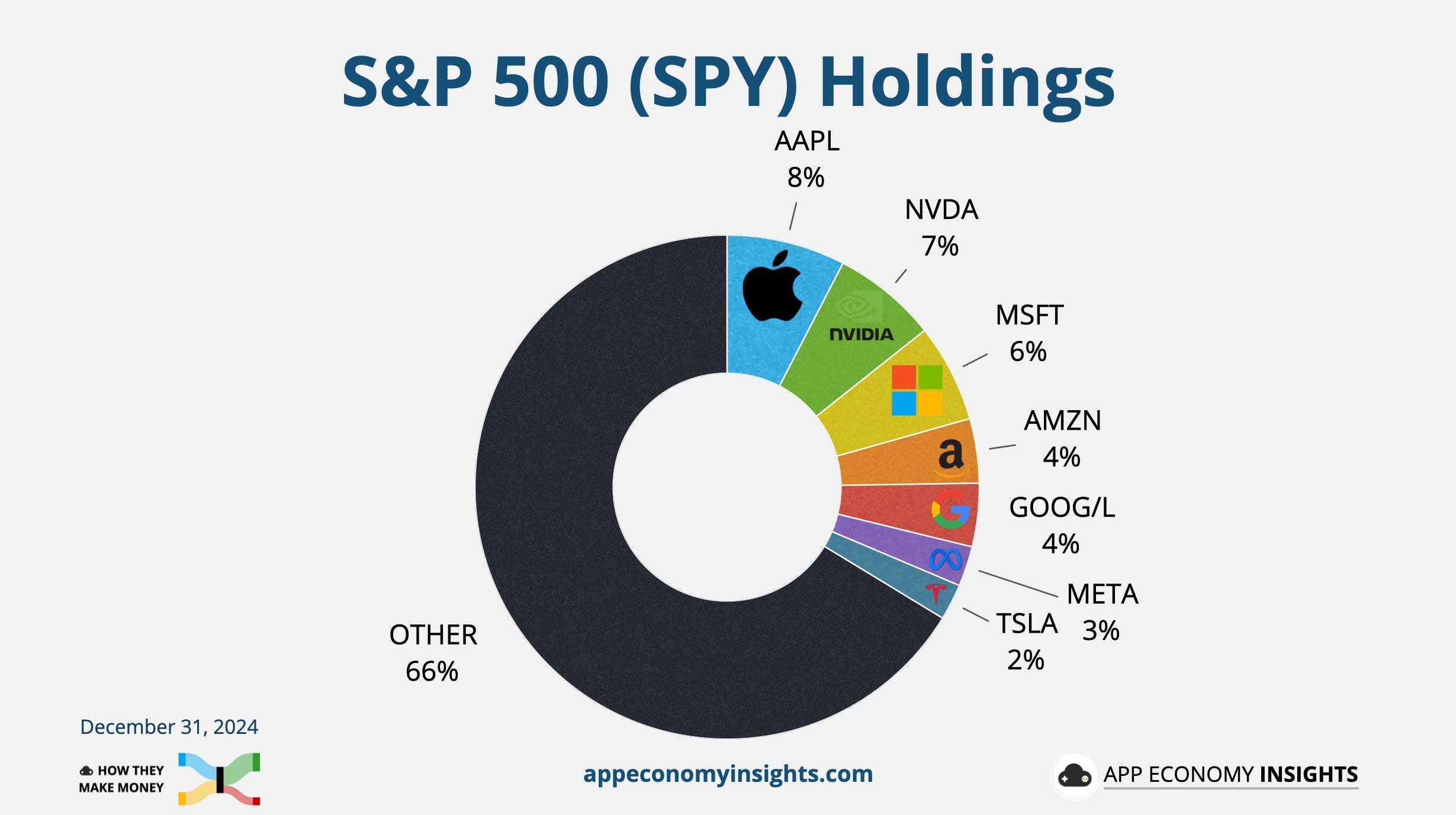

Another very interesting fact is that financial markets have gradually shifted from active investing to passive investing, largely due to the rise of market-cap-weighted ETFs. In this model, the larger your market cap, the more ETF allocation you receive. Strategy can strategically use its ATM program around ETF inclusions or rebalancing events. The buying pressure from ETFs can offset the dilutive effects of ATM issuance. As Strategy issues more shares, its market cap grows, triggering more ETF demand, allowing for further ATM issuance — a self-reinforcing cycle. Last year, Strategy announced a $21 billion ATM and $21 billion debt capital structure. During the Q4 of 2024, it issued over $15 billion in equity(a size never seen before), coinciding with its inclusion in the QQQ ETF. The next major catalyst is likely to be S&P 500 (SPY) inclusion, anticipated this September — another potential trigger for significant Bitcoin accumulation.

Figure 22: SPY is heavy weighted by large cap tech stocks. Source: APP Economy Insights

Risks to the Strategy Model

The main risk to the Strategy flywheel—and arguably the only one that matters long-term—is if Bitcoin’s internal rate of return (IRR) falls below the company’s cost of capital. If Bitcoin returns less than 10% annually, preferred equity holders (like STRK or STRF) would earn more yield than the BTC is generating, making it impossible to create value for common shareholders. The same applies to convertible bonds: typically structured over 4–5 years, they rely on BTC compounding above 10% to convert accretively. Otherwise, Strategy is left with debt and no increase in Bitcoin per share. In such a scenario, the company’s leverage ratio becomes critical. High leverage paired with weak BTC performance can create financial strain—even without margin calls—due to future repayment risks or increased dilution. One cycle is survivable, but if Bitcoin underperforms across multiple cycles, the flywheel breaks. The model only works if Bitcoin consistently outpaces the cost of capital used to acquire it. Lastly, Strategy’s brand and investor confidence are closely tied to Michael Saylor. His leadership and Bitcoin advocacy are central to the company’s identity. Any departure, health issue, or reputational damage could erode trust, impair capital access, and threaten the mNAV premium that powers the flywheel.

Global Opportunity: The Rise of Bitcoin Treasury Corporations

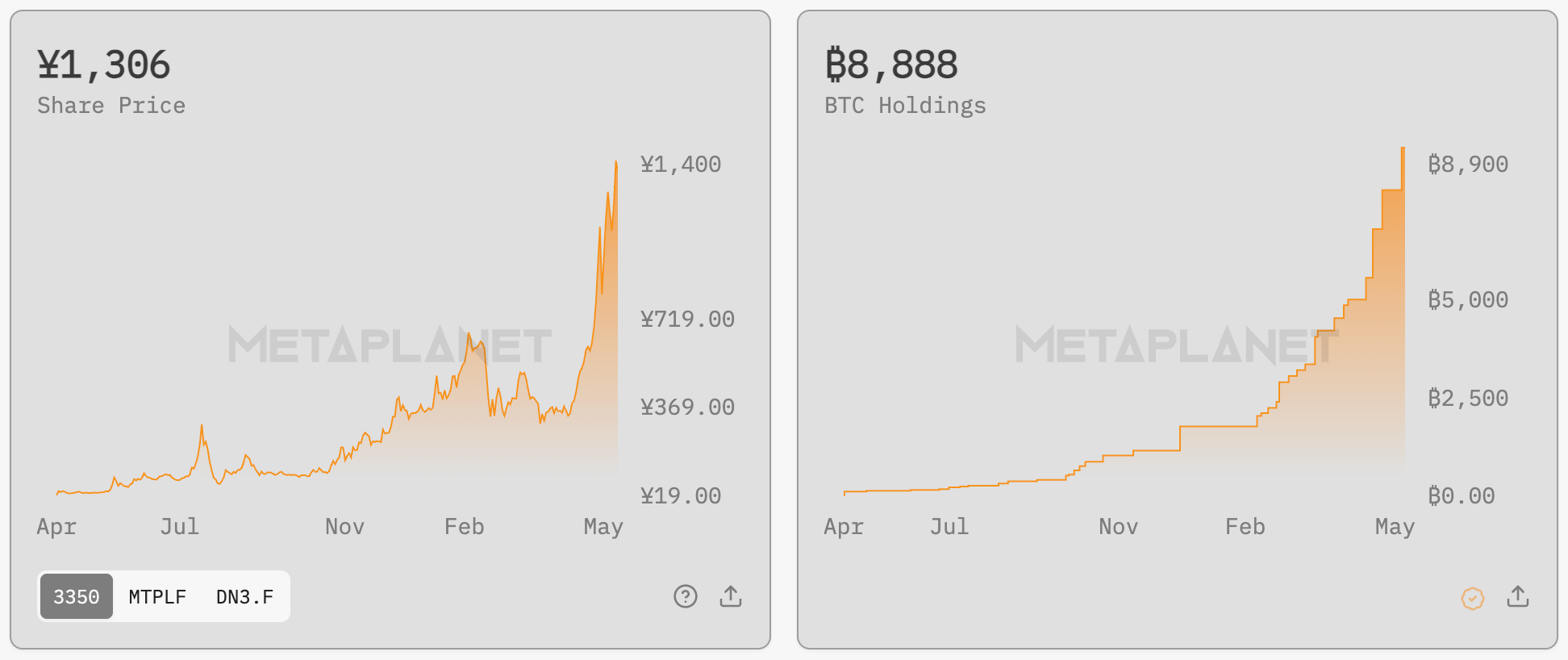

Looking ahead, due to varying regional financial regulations, we may see the emergence of local analogues to Strategy — firms that offer Bitcoin exposure through equity structures tailored to their domestic regulatory environments. A notable example is Metaplanet, which is positioning itself as Japan’s version of Strategy and could become a key player in this evolving landscape due to Japan’s low cost of capital and yield starving financial environment.

Figure 23: Metaplanet’s stock price action and Bitcoin holding change over time, showcasing massive success in the replication of Strategy’s playbook in Japan. Source: Metaplanet

Other Asset Treasury Company: Does it work?

Recently, there has been growing interest in creating “Strategy equivalents” for Ethereum or Solana. But from a first-principles perspective, the viability of such a model depends on whether institutions are willing to buy convertible bonds or preferred equity backed by those assets. In reality, that appetite is extremely limited. Without institutional funding mechanisms, these companies would be forced to rely on secondary equity issuance via ATM programs—dilutive by nature and ultimately unsustainable without capital-efficient instruments.

Crucially, the IRR of non-Bitcoin crypto assets is uncertain and lacks institutional trust. Without a credible expectation that ETH or SOL can reliably outperform the yield on structured products, capital allocators are unlikely to back this model. In short, Strategy’s strategy is uniquely enabled by Bitcoin’s properties—and is unlikely to be replicable elsewhere at scale.

Part 4: Key Metrics to Track for Strategic Accountability

As one can see, equity issuance is at the core of Strategy’s strategic flywheel. Therefore, tracking the right metrics is essential to understanding the sustainability and effectiveness of this model. Four key metrics stand out:

Bitcoin per Share: This is calculated by dividing the total amount of Bitcoin owned by the company by the fully diluted share count — which includes shares from convertible bonds, options, and RSUs/PSUs. Using the fully diluted share base ensures consistency and reflects the true potential dilution. This metric shows how much Bitcoin effectively backs each share. If Strategy is issuing equity at or below an mNAV of 1, the issuance is not accretive to Bitcoin per share.

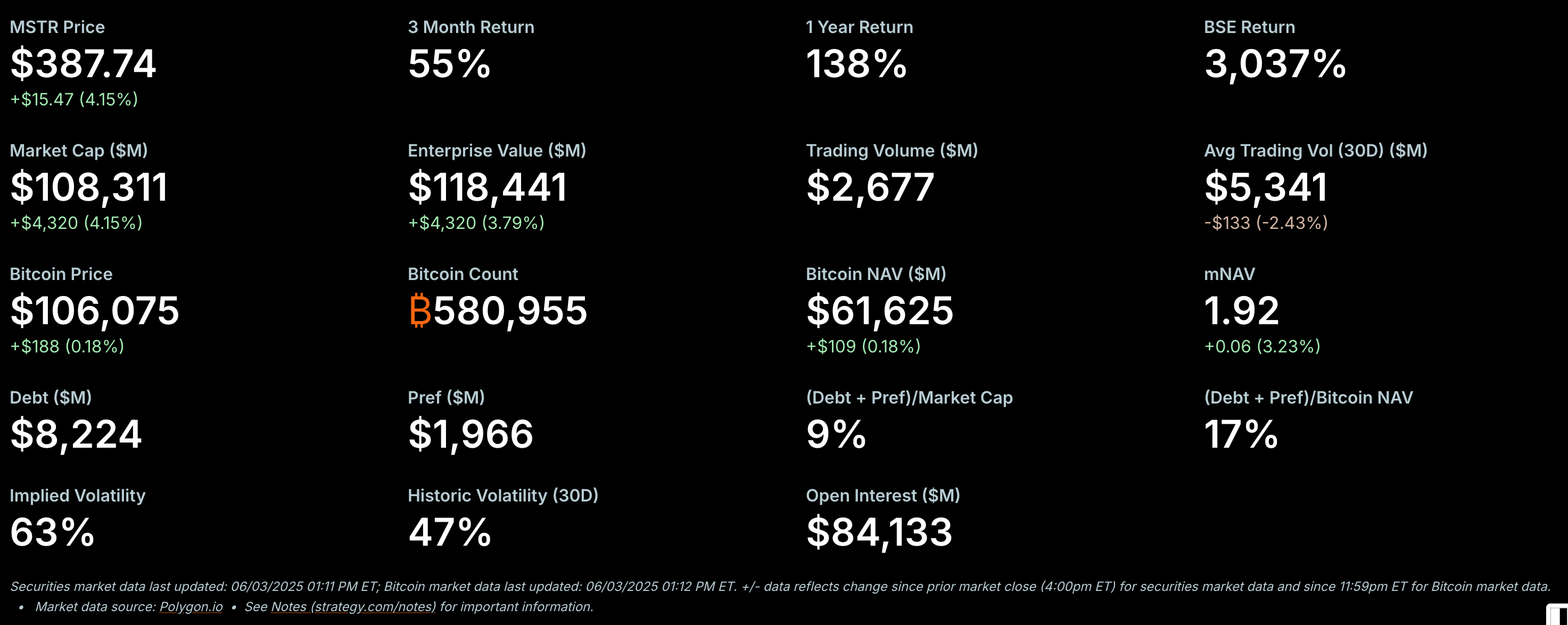

mNAV (Multiple to Net Asset Value): This is the market value of a share relative to its net asset value. A higher mNAV enables the company to issue equity at a premium, increasing its Bitcoin holdings per share. For reference, MSTR currently trades at an mNAV of approximately 2.24.

mNAV = Market Price per Share / (Total Assets – Total Liabilities) ÷ Total Shares Outstanding

Bitcoin Yield: This metric measures the change in Bitcoin per share over time. It is typically updated quarterly or annually to align with earnings reports, but may also be updated immediately following material Bitcoin purchases. Bitcoin Yield reflects how efficiently the company converts capital raised into increased BTC backing per share.

Leverage Ratio (%): This is the ratio of total debt to the fair market value of the company’s Bitcoin holdings. It indicates how much financial risk is present on the balance sheet. Strategy targets a leverage ratio in the 20–30% range, generally operating near 25%. This allows for some volatility in Bitcoin’s price while maintaining financial discipline.

Part 5: BTC Credit Rating Framework

To bring clarity to its balance sheet, Strategy created a BTC Credit Rating framework. This measures how much Bitcoin backs each liability by comparing the BTC NAV to the liability’s notional value:

BTC Rating = BTC NAV ÷ Liability Notional

A higher rating means more collateral and lower risk. If the rating falls below 1x, the liability is undercollateralized. To quantify this risk, Strategy calculates BTC Risk—the chance that BTC Rating drops below 1x over the life of the instrument—based on expected BTC volatility and return.

That risk is then translated into an annualized BTC Credit Spread:

If this spread is under 100 bps, Strategy considers the instrument investment grade, even if markets price it otherwise. For example, STRF has a BTC Rating of 5.8x and just 1% BTC Risk at 30% BTC ARR—translating to a BTC Credit Spread under 100 bps.This framework helps Strategy benchmark BTC-backed liabilities against traditional credit, making the case for eventual credit agency recognition—and revaluation of MSTR preferred equities.

Part 6: Business Model - A Value-Generating Machine in the Era of Rapid Bitcoin Institutionalization

Strategy is, at its core, a Bitcoin security company, as outlined above. Its business model is novel and structurally unique in public markets. It has three key advantages:

Scalable Access to Capital with Low Cost: Strategy can raise capital efficiently through instruments like convertible bonds and preferred equity. While these carry future obligations (such as interest or dilution), the company incurs minimal immediate cash costs and low interest cost. This capital efficiency enables rapid Bitcoin accumulation without the traditional constraints of operating cash flow or profit generation.

Pro-Competitive and Positive-Sum: The model benefits from broader adoption. As more companies pursue similar strategies, overall demand for Bitcoin increases, thereby driving up its price. In this ecosystem, competition is not a threat — it creates a super positive sum game.

High Margin for Error: Because Strategy relies on long-term, uncallable liquidity, it operates with a high margin for error. Even if the timing or execution of share issuance is suboptimal, the company isn’t forced to act under pressure. As long as Bitcoin appreciates over time, simply doing nothing and being patient can still result in success.

Part 7: Reform to Modern Portfolio Management

As Jeff Park aptly illustrates, “the traditional 60/40 portfolio split—60% in equities for growth and 40% in bonds for safety—has reached the end of its relevance.” Bonds were traditionally expected to hedge equity risk, especially during economic downturns or risk-off periods. Moreover, they have long been viewed as a partial hedge against inflation. While cash held in banks loses purchasing power over time, treasuries at least offer a mechanism to preserve value—albeit imperfectly.

However, since 2020, the bond market has increasingly diverged from its historical role as a hedge against equity risk. This was clearly evident in 2022, when the S&P 500 (SPY) declined by 18% and treasuries also fell by 13%, failing to offer the expected protection. This trend has persisted into 2024. Additionally, during the recently tariff turmoil—when SPY and QQQ experienced a sharp selloff—treasuries and USD were not bought up as a safe haven. Instead, yields surged to nearly 5%, further indicating that treasuries no longer act as a reliable risk-off hedge.

Figure 25: SPY correlation with treasuries on an annual basis. Source: Bloomberg, X@jeffpark

There are two primary reasons for this shift. First, global equity markets have become increasingly driven by liquidity rather than fundamentals. Economic slowdowns now often prompt massive government intervention and monetary expansion, which in turn drives treasury prices down rather than up. Second, the credibility of the U.S. government’s ability to meet its debt obligations has come under scrutiny. The freezing of Russian assets and a broader move toward deglobalization have raised concerns globally, prompting investors to diversify away from U.S.-backed assets. Concurrently, the rapid rise in U.S. debt has eroded confidence in both the dollar and treasury securities. As a result, during risk-off periods, global portfolio managers are less inclined to reflexively shift capital into U.S. treasuries.

As mentioned at the beginning of this report, inflation often manifests more prominently at the asset level. Traditional treasuries yielding 0–5% do not effectively hedge against real inflation, especially since the CPI basket of goods evolves over time. In contrast, Strategy’s preferred equities offer a novel fixed-income product—essentially, a bond backed by a true inflation hedge: Bitcoin. These preferred shares generate dividends tied to an 8% Bitcoin-backed return (with an additional 2% stemming from preferences related to STRF and STRD). In essence, Strategy has created a real-world application of Bitcoin as a store of value within the traditional finance (TradFi) system—an innovation that is just revolutionary.

While the U.S. fixed income market is valued at approximately $46 trillion, the global fixed income market surpasses $150 trillion. Capital in the fixed income space has become increasingly commoditized—performance and yield are now the key differentiators. In portfolio construction, asset managers are often willing to accept slightly higher risk in exchange for higher returns. While it may take time to educate the market on Strategy’s preferred equity as a viable fixed-income product, it’s not unrealistic to envision it capturing 1% of global bond allocations. If Strategy were to achieve this, it could translate into $1 trillion in potential capital—liquidity that could be deployed into Bitcoin. The impact of such a shift is hard to quantify. I can’t say how high MSTR or Bitcoin would go, but one thing is clear: higher.

Closing Remarks:

I’d like to extend my sincere thanks to Brian Brookshire—not only for his thoughtful feedback on this piece, but also for his guidance in helping me understand the intricacies of Strategy’s playbook. He’s one of the most insightful MSTR analysts out there, and if you’re interested in this space, I highly recommend giving him a follow. If you found this write-up valuable, please consider liking, sharing, and subscribing to Artemis Substack, following on X, and connecting with me on X. Your support truly means a lot!