Ethereum FY 2023 Financial Overview

an in-depth look at Ethereum through the lens of a financial analyst

This article aims to offer a comprehensive analysis of Ethereum through the lens of key financial and operational indicators. Additionally, it will present valuation frameworks that benchmark Ethereum's fundamental metrics against those of other blockchain networks.

All analyses based on Artemis data - link to excel back-ups at the end!

Ethereum Key Takeaways

Ethereum Relative Valuation Analysis

Ethereum FY 2023 Highlights

Ethereum FY 2023 Key Financial Metrics

Conclusion

Ethereum Key Takeaways:

DeFi was the largest driver of gas usage in FY 2023, generating ~$776mm of transaction fees for Ethereum (32% of total network fees)

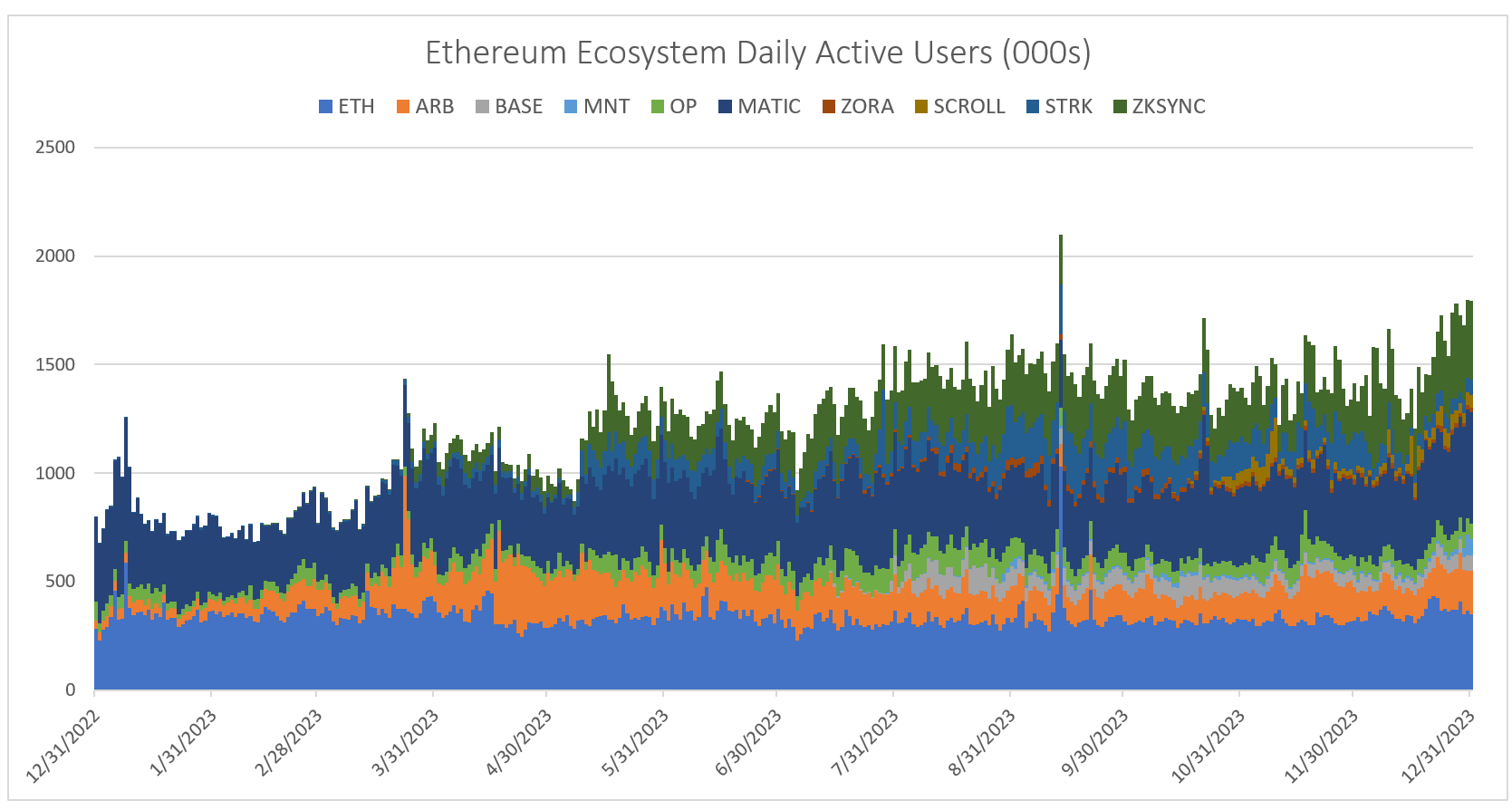

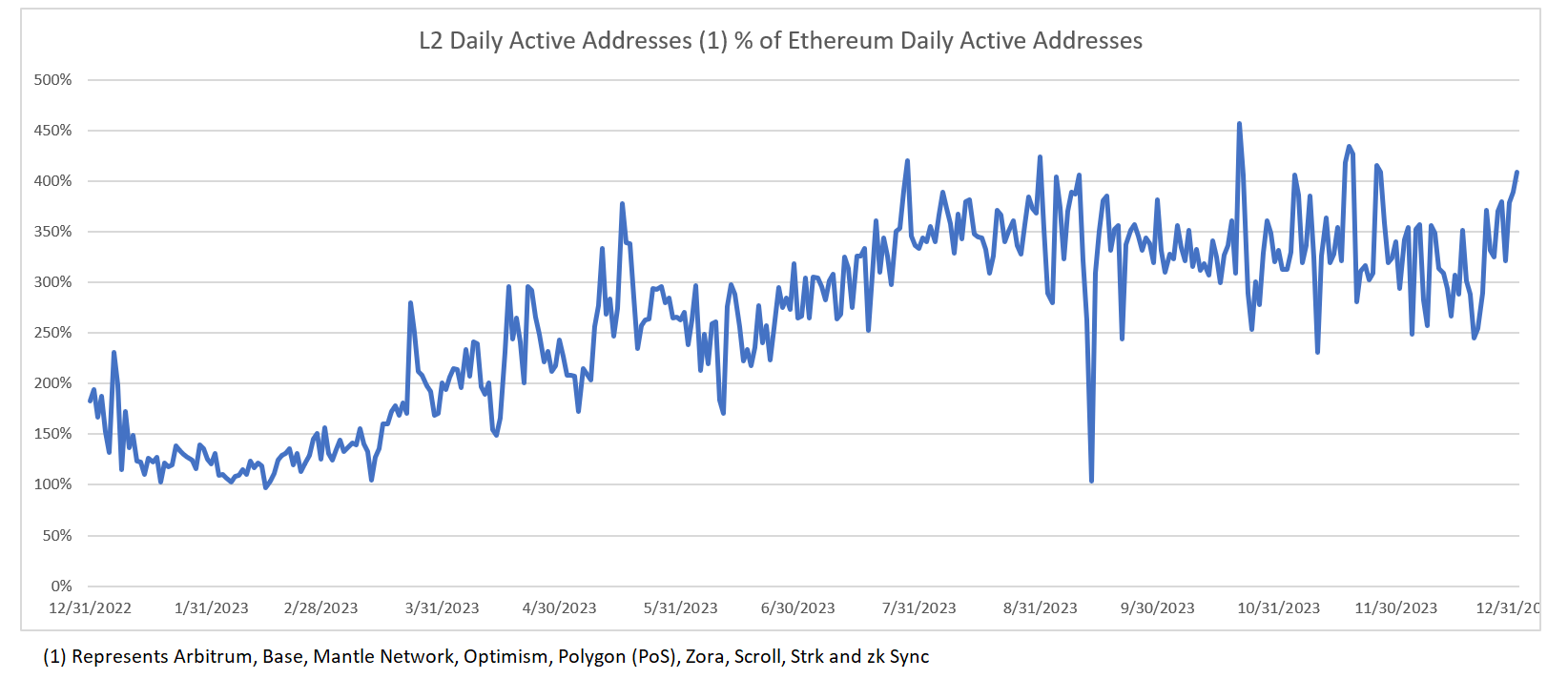

User activity continues to move to layer 2s, with Layer 2 daily active addresses making up ~400% of Ethereum daily active addresses

Ethereum is seeing a wave of new drivers for transactions fees on the network

DeFi transaction fees grew YoY in 2023 driven by new DeFi primitives (e.g. telegram trading bots) and the continued dominance of Uniswap (~30% YoY growth)

(1) New DeFi primitives driving gas usage: Maestro is a telegram trading bot allowing users to “snipe” new DEX pools and purchase tokens as soon as liquidity is provided into a pool. The application drove ~$28mm in fees after its latest contract deployment launched in Q4 2023 (ending the year as a top 5 gas-consuming DeFi app on Ethereum)

Uniswap is still king, generating ~67% of gas usage attributable to DeFi in FY 2023

(2) Layer 2s have seen remarkable growth over the past year, with Ethereum transaction fees attributable to layer 2s growing ~105% YoY in 2023 to ~$150mm. zkSync and Arbitrum were the largest layer 2 networks in terms of gas consumption with ~$56mm and ~$50mm of transaction fees paid to Ethereum L1 in FY 2023, respectively

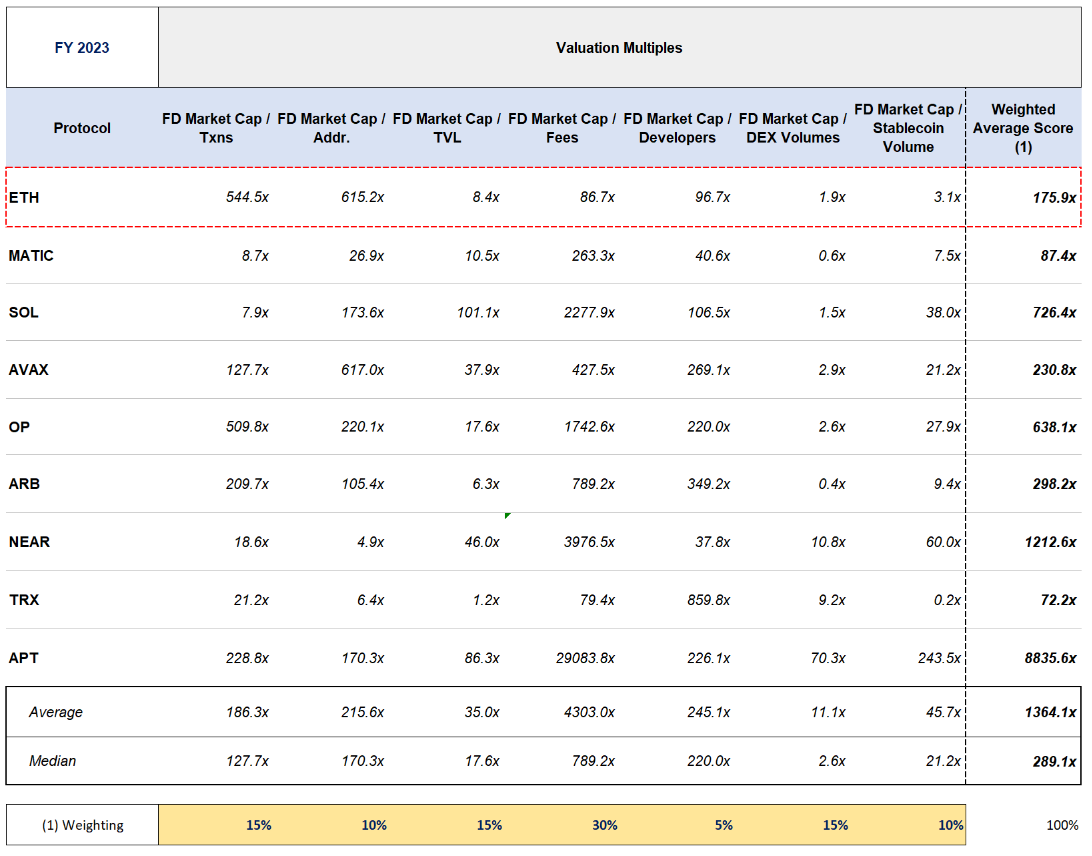

Ethereum Relative Valuation Analysis:

As the crypto asset class matures, we believe that investors will increasingly evaluate blockchain networks such as Ethereum through the lens of fundamental metrics. At Artemis, we have begun to piece together ways to evaluate blockchain networks using a set of standardized metrics

We have taken into account relevant fundamental metrics such as On-chain Transactions, Daily Active Addresses, TVL, Transaction Fees, Developers, DEX Volumes and Stablecoin Volumes. We created a weighted average score that placed heavier consideration on fundamental metrics that we believe provides a lens into the health of a blockchain network (Fees, DEX Volumes, transactions, TVL). We’d love to get thoughts and feedback on our methodology!

Valuation Summary:

As of FY 2023, Ethereum trades below the median of its peers on the weighted average score that Artemis has constructed, with only MATIC and TRX trading at lower multiples

Ethereum trades near the bottom of its peer group on a FD Market Cap / Fees basis (only TRX trades lower) and on a FD Market Cap / Stablecoin Volume (again only TRX trades lower)

While Ethereum doesn’t necessarily look cheap on all dimensions (i.e. its FD Market Cap / Addresses), trades below both the average and median weighted average multiples of its peer group

In the future, we recognize the need to include the impact of the growing Ethereum Layer 2 ecosystem as part of the fundamental lens with which to view Ethereum. At this time, the only fundamental metric attributable to the layer 2 ecosystem that impacts our analysis is Fees (Layer 2s pay gas to Ethereum L1 to post data, as Layer 2 network usage increases, transactions fees on Ethereum L1 increases)

Ethereum FY 2023 Highlights:

Ethereum’s FY 2023 Total Transaction Fees of $2.4bn declined 44% YoY vs. $4.2bn in FY 2022

FY 2023 saw 339k average daily active addresses, down ~10% YoY from 377k in FY 2022

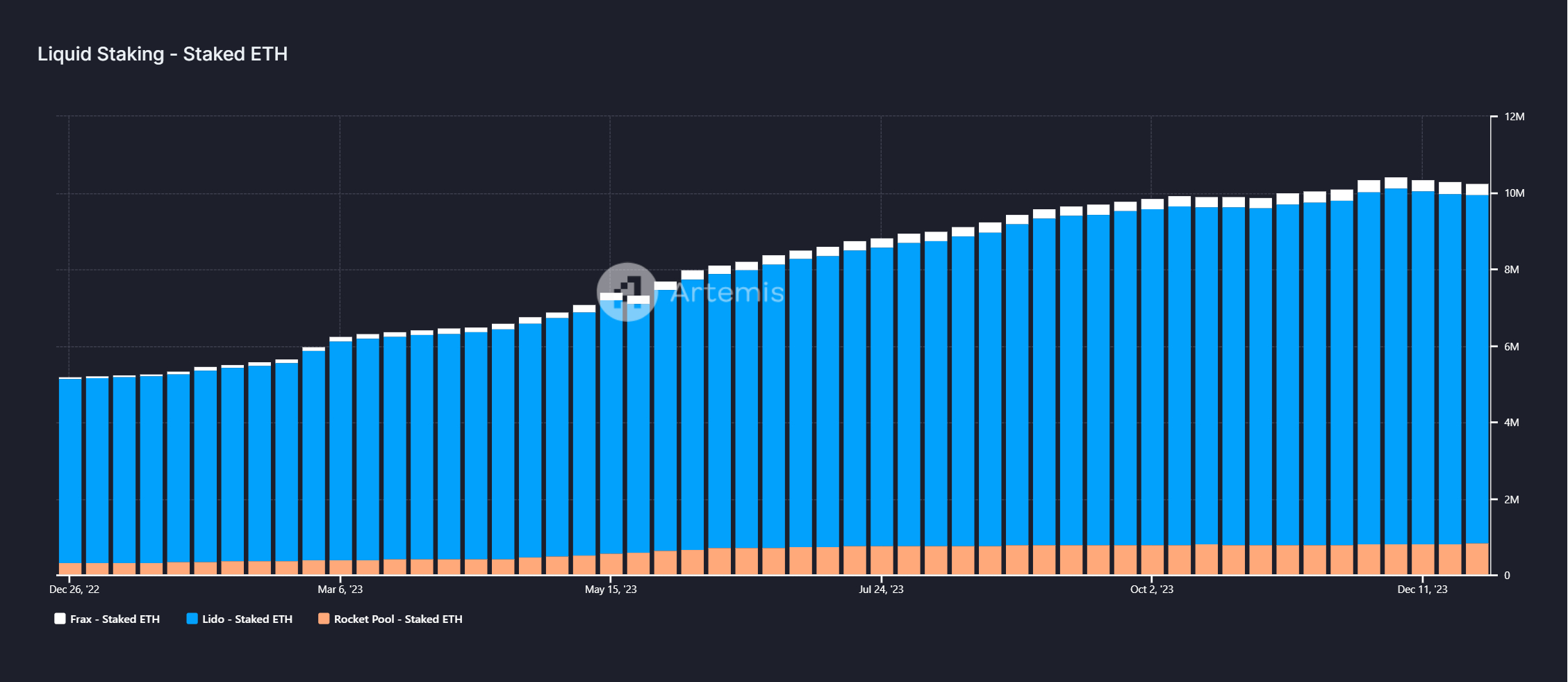

ETH Staked grew 119% in 2023 to 32.9mm tokens staked, equating to ~27% of Ethereum’s total circulating supply

Ethereum TVL declined slightly in USD terms from $26.1bn at FY 2022 to $25.2bn at FY 2023

FY 2023 marked the first full year after the completion of the Merge in Q3 2022, moving Ethereum to a Proof of Stake Blockchain. This has pushed Ethereum to a deflationary state in FY 2023 for the first year in its history

User Metrics:

Total Ethereum transactions fell 6% vs. FY 2022 to 383mm, but those figures do not tell the full usage story. The layer 2 ecosystem has come into full force with eight different scaling solutions boasting 50k+ daily active addresses (with MATIC tracking at ~400-500k daily active addresses)

We are also able to evaluate the growth in the layer 2 ecosystem by calculating how much layer 2 active addresses have grown as a % of Ethereum daily active addresses. From this analysis, we can see that Layer 2 daily active addresses as a % of Ethereum daily active addresses grew from a trough of ~100% in January 2022 to more than ~400% at the end of January 2023. We expect the trend of usage moving to layer 2 solutions to continue, as solutions enabling the efficient deployment of roll-ups arrive on the market (i.e. Celestia, Eigenlayer)

Passive Economic Capital:

ETH staked grew double digits QoQ in 2023 to ~28.4mm ETH staked

ETH staked as a % of total circulating supply increased from 7% at FY 2022 to 24% at FY 2023

Liquid staking platforms continued to grow in 2023 with Lido growing from 4.8mm ETH staked in December 2022 to 9.2mm in December 2023

Ethereum saw Total Value Locked (TVL) fall over FY 2023 from $47.6bn average balance in 2022 to $25.8bn in FY 2023 (~46% YoY decline)

Similar to usage metrics, this doesn’t necessarily tell the entire story given that layer 2 scaling solutions have also begun to accrue TVL. Over the course of 2023, we have seen networks such as Arbitrum and Optimism grow to $1bn+ of TVL

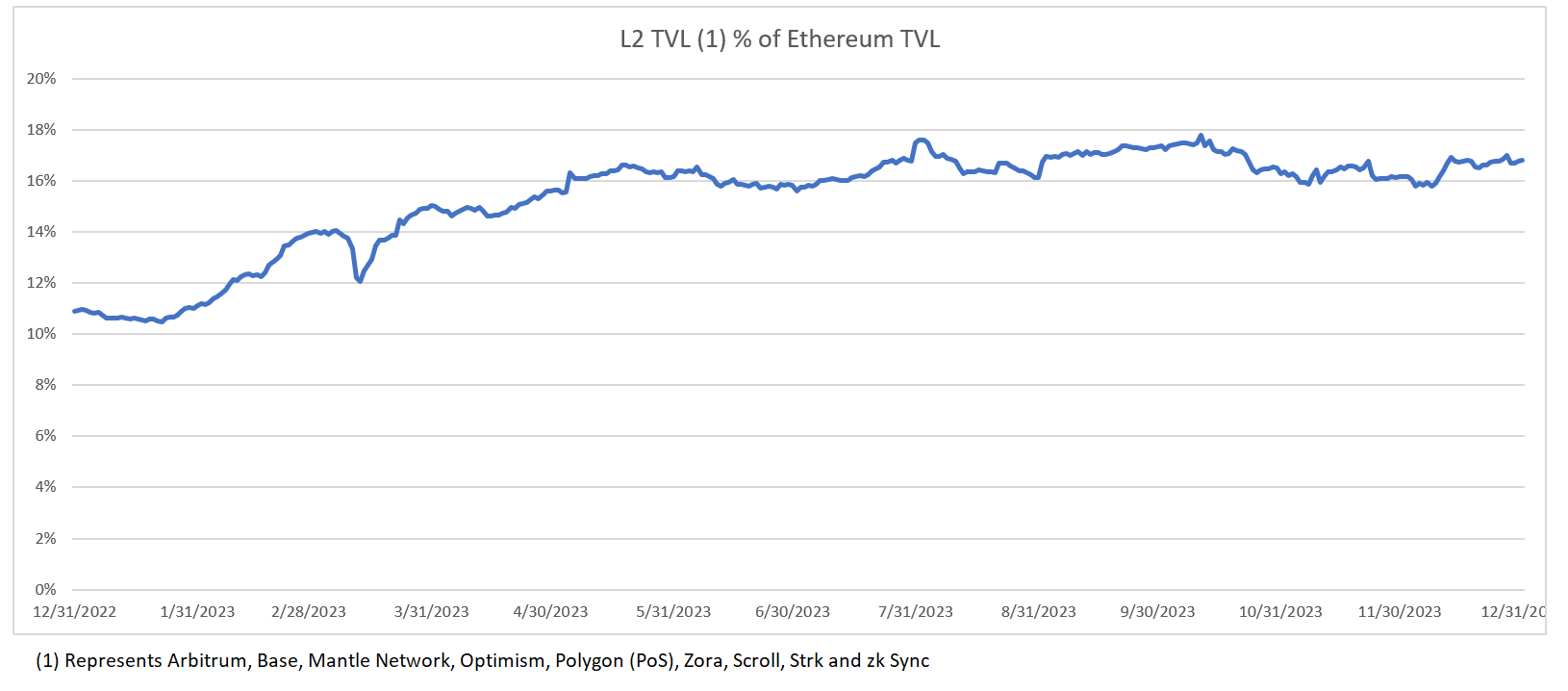

L2 TVL has similarly continued to climb as a % of Ethereum TVL over the course of 2023, growing from ~11% at December 2022 to ~17% at December 2023

Ethereum FY 2023 Key Financial Metrics:

Ethereum generated ~$2.4bn in total transaction fees in FY 2023 (1.31mm ETH), down ~44% vs. FY 2022 total transaction fees of $4.2bn (1.76mm ETH). Transaction fees represent the total amount of gas utilized by consumers to execute transactions on the Ethereum blockchain

2023 marks the second year of continued decline in total transaction fees in both native ETH and USD terms, but the first year that the ETH was net deflationary. This was due to the completion of the Merge in Q3 2022 which moved the Ethereum blockchain to a Proof of Stake network

$2bn of transaction fees were burned in FY 2023 (down 45% YoY) and 1.09mm ETH were burned (down 26% YoY in native token terms). The difference is due to fluctuations in the Ethereum token price

84% of transaction fees were burned in 2023, the same percentage burned in 2022

Ethereum ended the year with ~1.1% deflation, indicating that more tokens were burned than were issued in FY 2023

2023 marks the first year that the Ethereum network was deflationary, after seeing high single digit / low double digit inflation in the prior two years

Ethereum Transaction Fees - Sector Level Detail:

What were the largest drivers of transaction fees on Ethereum in 2023? Artemis breaks down fees by constituent categories:

Summary

DeFi remained the largest sector on Ethereum in 2023 generating $776mm of transaction fees. DeFi spiked in Q2 2023 alongside the USDC depeg following the collapse of SVB, and ended the year up vs. FY 2022 fees in USD terms

Total fees continued to decline YoY in USD terms, driven by softer USD prices as well as lower levels of network usage

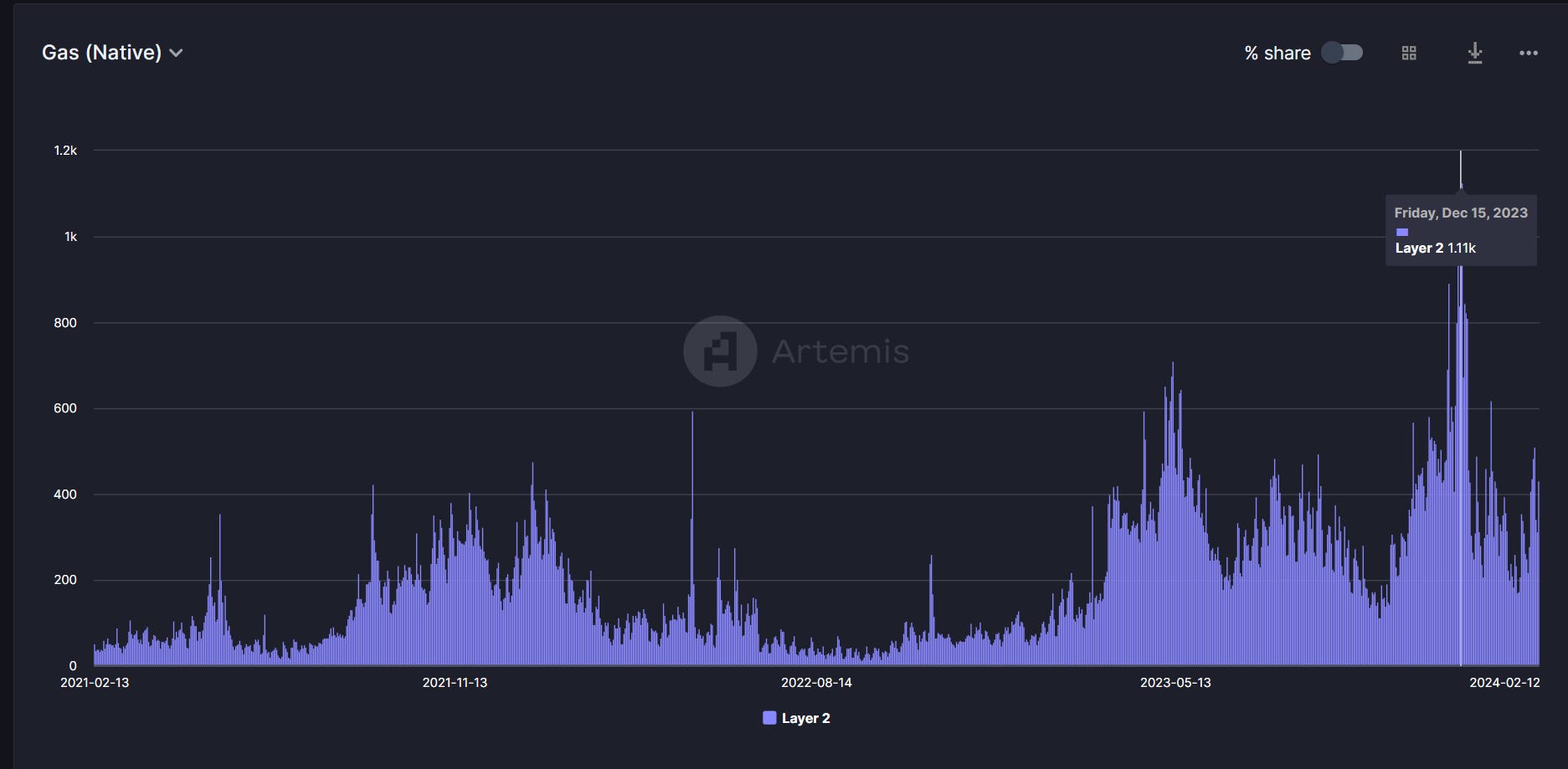

Layer 2 gas usage grew meaningful over the course of 2023 particularly in native token terms. Gas in native ETH tokens has already eclipsed the peaks of 2021 through the launch of new blockchain networks

Wallet transfers of both stablecoins and the native ETH token saw gas usage decline ~50%+ in FY 2023, while NFT related applications (e.g. NFT marketplaces) also saw a ~76% decline in 2023

DeFi:

The top five applications generated ~80% of total DeFi gas usage in FY 2023. There is a substantial power law in effect within the DeFi space, with the top few applications generating the vast majority of transaction fees on Ethereum

Uniswap was the largest consumer of gas by a wide margin, making up ~83% of DeFi gas usage

Telegram trading bots took the world by storm in FY 2023. The latest contract deployment of telegram trading bot Maestro launched in Q4 2023 (Router 2) and became one of the top 5 highest fee consuming applications on Ethereum

OneInch and 0x Exchange, decentralized exchange aggregators, along with Lido, the largest liquid staking derivative protocol on Ethereum rounded out the other top DeFi applications on Ethereum

Layer 2 Networks:

The top five layer 2 networks saw 119% growth in average daily active users in FY 2023. The year saw a number of new blockchain launches including zkSync (640k average daily users) and Base (119k average daily users). Existing blockchains including Arbitrum and Optimism also saw an explosion in growth in 2023, hitting 594k and 283k average daily users, respectively

The top 5 layer two networks also saw their contribution to Ethereum gas usage increase 105% in 2023, indicating higher demand for Ethereum blockspace to post data costs

The top 5 layer 2 applications generated $208mm of transaction fees (fees paid directly to the layer 2 platform, not accrued to Ethereum L1) and grew a whopping ~218% YoY in FY 2023

After subtracting the gas that these layer 2 applications pay to Ethereum L1 (the cost of posting / preserving transaction-level data), all of the layer 2 applications saw a positive profit margin in 2023, after seeing negative margins in 2021 and 2022. This is because the layer 2 applications benefit from operating leverage, where higher transaction volumes translate into higher fees / profits for the layer 2 without a corresponding increase in costs

Conclusion

The Ethereum network now has multiple years of history with real fundamental metrics to evaluate. As the crypto industry continues to mature, we will continue to refine the operational and valuation standards that will help shape how investors think about the digital assets space.

While some headline metrics appear to be flat to down for Ethereum in FY 2023 (average daily users down ~10% YoY, total fees down ~44% in USD terms), there are numerous bright spots that suggest continued growth within the Ethereum ecosystem:

Growth in new product categories: We have seen new innovations within the consumer social space with Farcaster recently hitting 40k DAUs in February 2024. The protocol has generated ~600k revenue to date since its launch in Q3 2024, and its usage will contribute to contribute to transaction fees on its layer 2 network BASE as well Ethereum L1

Continued maturation of Ethereum’s layer 2 ecosystem: FY 2023 saw the layer 2 ecosystem come into full force with multiple networks generating more daily active users than Ethereum. We expect this trend to continue as more consumer facing applications deploy on layer 2 networks

EIP 4844 Upgrade: Ethereum is also expected to make an upgrade to its infrastructure in Q2 2024 called EIP-4844. With this upgrade, Ethereum is moving towards adopting an architecture called sharding. This will add a data layer (holding storage) that will interact with the execution client (the EVM) and other L2 chains. The main benefits of this EIP will allow for reduced transaction fees for layer 2 rollup solutions, further reducing gas fee costs for layer 2 blockchains

Digital asset and stablecoin regulation: Digital asset regulation and acceptance by traditional financial institutions was a bright spot for crypto in 2023. After the SEC allowed for the launch of BTC ETFs in January 2024, BlackRock and Fidelity have accumulated a combined ~$5.5bn in Bitcoin. Additionally, as stablecoin regulation comes into effect in various international jurisdictions (Europe, Japan, Hong Kong, Singapore) we expect stablecoin transfers will drive higher levels of gas usage on public blockchains such as Ethereum

And that’s all folks - we’ll continue to build upon this analysis, but please feel free to reach out with any questions or thoughts! We’d love to hear from you.

Links to back-up analyses:

Thanks to Sam Andrew at North Island Ventures for his thought work and serving as part of the inspiration behind this piece.