Artemis Weekly Wrap-up (8/26/2023)

your go-to source for weekly fundamental updates

This week, the US Treasury Department released a proposal on how to handle crypto tax reporting and Tornado Cash developers were charged for helping hackers launder ~$1bn+.

let’s jump right in 👇

🌞 Coinbase takes stake in stablecoin issuer Circle

💫 Artemis Data Insight #1: YTD Ethereum Gas Usage

🤝 Artemis Data Insight #2: Optimism vs. Arbitrum Gas and User Activity Comparison

The market continued to churn lower across the L1 / L2 universe with average and median WoW price drops of ~3.1% and ~3.7%, respectively, while equity markets inched upwards (S&P 500 and NASDAQ index up ~0.7% and ~1.9% over past 5 days, respectively). Bitcoin fell below $26k after the crypto markets reacted to hawkish statements by Jerome Powell committing to raise rates further if appropriate in a continued effort to contain inflation.

🌞 Coinbase takes stake in stablecoin issuer Circle

Coinbase and Circle, two major players in the cryptocurrency world, have jointly announced new developments surrounding their collaboration on the USD Coin (USDC). Over the years, USDC has cemented its role in the crypto landscape, evolving into the second-largest stablecoin in the global market with a ~$25bn market cap (Defillama). Coinbase has now announced that it intends to take a minority stake in Circle, allowing revenue to be shared based on the amount of USDC held of each respective platform. Both companies have confirmed that they will continue to share revenue derived from USDC reserves interest income, which has become a significant contributor to Coinbase’s financial performance given borrowing rates near 15-year highs (Coinbase recorded $151mm in revenue from USDC in Q2 2023).

USDC is now set to expand its reach by launching on six additional blockchains between September and October. This move, increasing its multi-chain integration to 15, aims to bolster its appeal to a broader swath of developers around the globe.

Circle and Coinbase, as co-founders of the stablecoin, had initially set up the Centre Consortium to oversee USDC's governance. However, with increasing regulatory clarity emerging for stablecoins both in the US and internationally, Circle and Coinbase have made the decision to dissolve the Centre Consortium. Circle will retain sole control over USDC issuance and governance, centralizing operations and enhancing accountability, including compliance with regulations and enabling USDC on new blockchains.

💫 Artemis Data Insight #1: YTD Ethereum Gas Usage

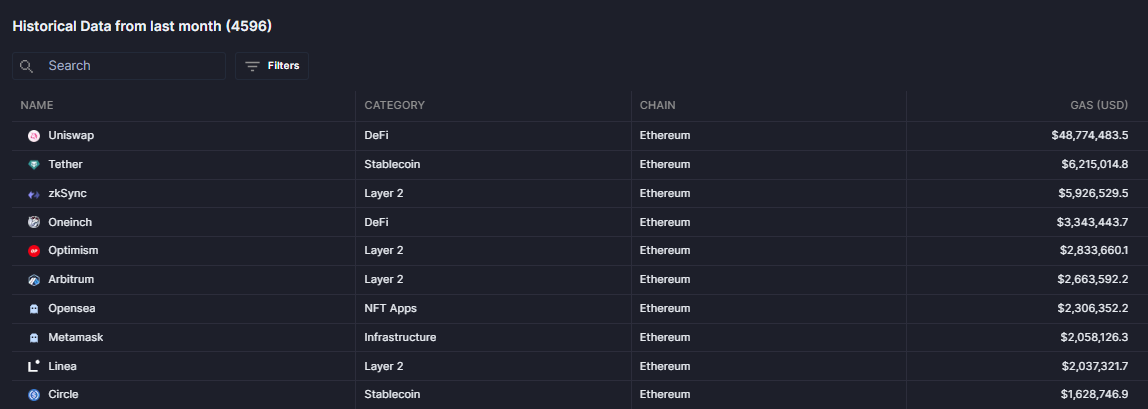

Ethereum has ~$1.6bn in gas usage year to date (August 24, 2023). What are the largest categories and applications that make up that usage?

Based on data from the Artemis Blockchain Activity Monitor, we can see that the some of the largest components of Ethereum gas usage include DeFi (DEXs), Stablecoins and Layer 2 solutions. Uniswap remains the #1 application by gas usage with ~$49mm of gas consumed over the last 30 days, which made up ~30% of total gas usage of Ethereum over the same time period (~$170mm of gas consumed on Ethereum over last 30 days).

We have also seen the rise of layer 2s as a growing category of Ethereum gas usage over the past few months. Today, we see 4 different layer 2 solutions consuming $2mm+ of gas on Ethereum layer 1 over the past 30 days: Linea, zkSync, Arbitrum and Optimism. zkSync is the biggest gas guzzler out of the group, consuming ~$5.9mm gas over the past 30 days, and is cemented as the 3rd largest gas consuming application on Ethereum.

Other categories that make up the top 10 Ethereum gas guzzlers include stablecoins (Tether, Circle), NFT Applications (Opensea) and Infrastructure (Metamask). The Artemis team will continue to monitor how the top categories of Ethereum gas consumption evolve over time.

🤝 Artemis Data Insight #2: Optimism vs. Arbitrum Gas and User Activity Comparison

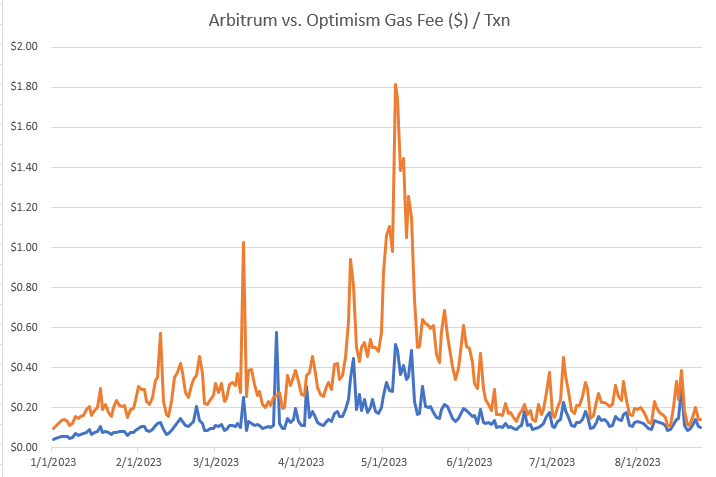

Arbitrum and Optimism have both become household names in the Layer 2 ecosystem. Today, we compare how the two ecosystems compare on the basis of gas usage, transactions and daily active users.

YTD - Arbitrum and Optimism have generated ~$40.1mm and ~$26.3mm in gas fees, respectively. Arbitrum has seen average daily addresses of ~152k in 2023 while Optimism has seen ~68k over the same period. This data tells an interesting story - while Arbitrum has 2.5x the number of users of Optimism, Arbitrum gas / txn and gas / DAA is actually meaningfully lower than Optimism over the YTD period.

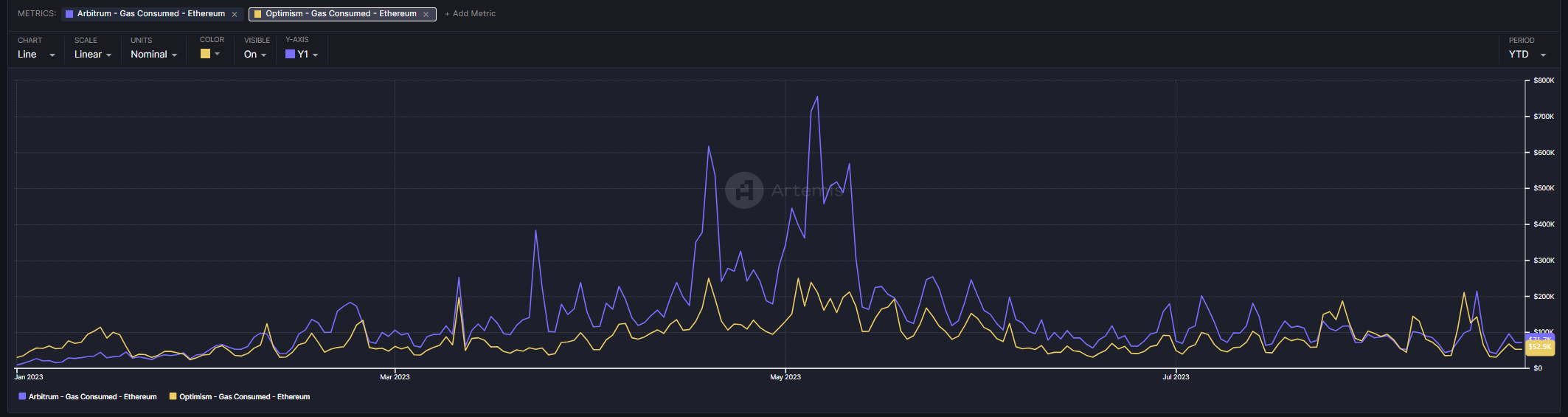

Finally, we looked at the gas costs that each respective application pays to Ethereum L1 for sequencing costs. YTD, Arbitrum paid $32.7mm in Eth L1 gas costs while OP paid ~$20mm.

Ultimately, while Arbitrum saw higher total gas fees on its L2 network, ARB actually saw a lower profit margin than OP did after accounting for ETH L1 costs.

YTD, Arbitrum and Optimism L2 Gas Fees less Eth L1 gas paid generated $8.0mm and $6.4mm of value, respectively. Ultimately, Arbitrum and Optimism have generated ~20% and ~24% profit margins after accounting for Eth L1 gas costs.

As the networks continue to mature and further Ethereum upgrades such as EIP 4844 come into play, we will continue to track how these figures evolve over time.

Detailed L1 dashboard for people who love more numbers in smaller font: